/perspectives/macroeconomic-research/the-economic-cycle-is-reaching-a-turning-point

Macroeconomic Update: The Economic Cycle Is Reaching a Turning Point

Leading signals are flashing red as the debt ceiling takes center stage.

First quarter real gross domestic product (GDP) growth was solid, with GDP excluding inventory swings growing at 3.4 percent annualized. The details showed that growth was bolstered by a sizable contribution from private consumption, which bounced back after a weak fourth quarter. Solid economic momentum was corroborated by other data, with the April purchasing manager indexes registering their strongest readings in several months. The labor market continues to hold up, with payroll job gains averaging 284,000 this year and the unemployment rate staying low at 3.4 percent as of April.

Below the surface, however, concerning signals are mounting. Jobs in cyclically sensitive industries are now falling, the leading economic index is in recessionary territory, continuing jobless claims have risen by 40 percent, and surveys of hiring plans point to a further slowdown in jobs growth. And this is all before the impact of a looming bank credit crunch has fully been felt and had time to flow through to the economic data.

Beyond the headwinds brought about by banking sector stress, we see several fundamental reasons to expect an economic slowdown as many growth tailwinds are also fading: the backfilling of jobs is winding down as the labor shortage eases; a construction backlog is clearing which should lead to headcount reduction; the growth boost from warm winter weather is over; excess savings are being drawn down, leading to rising reliance on borrowing to maintain consumption; and services consumption is back to trend. We still see a recession beginning in the second half of this year.

We do not expect the coming recession will be overly severe, as growth will likely be supported by housing bottoming as mortgage rates fall, auto production continuing to rise due to a multiyear backlog, and a better global growth picture aided by China’s reopening. Encouraging news on inflation means the Fed is likely on hold for the next few months as it assesses the cumulative impact of its rate hikes. Finally, the needed labor market rebalancing has so far been painless—with job openings down, quits down, and the labor force participation rate up—signaling that the ultimate increase in unemployment needed may be smaller than it appeared to be one year ago.

Markets are now turning their focus on the debt ceiling drama unfolding in Washington. While we don’t expect the worst-case scenario, the ongoing uncertainty and posturing around the deadline will keep investors on edge with tail risk becoming more elevated as the date approaches. A resolution or kicking of the can would be met with positive market reaction.

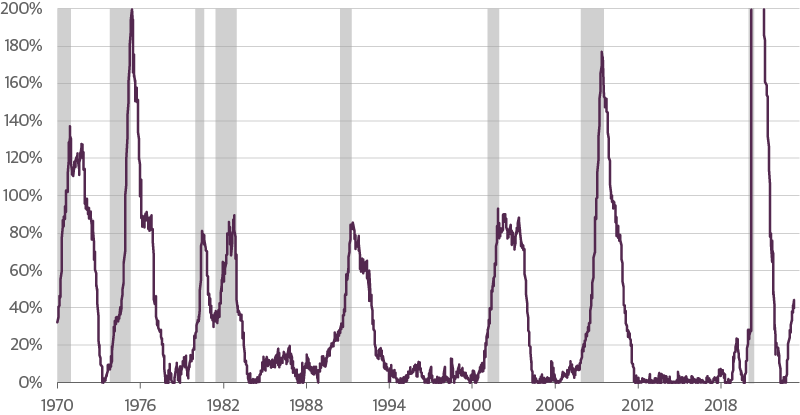

Jobless Claims Remain at Low Levels But are Rising Quickly

Continuing Jobless Claims, Increase from Trailing Three-Year Low

Concerning signals are mounting. Jobs in cyclically sensitive industries are now falling, the leading economic index is in recessionary territory, continuing jobless claims have risen by 40 percent, and surveys of hiring plans point to a further slowdown in jobs growth.

Source: Guggenheim Investments, Bloomberg. Data as of 4.29.2023.

—By Brian Smedley, Maria Giraldo, and Matt Bush

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the authors, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward-looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Investing involves risk, including the possible loss of principal. Investments in fixed-income instruments are subject to the possibility that interest rates could rise, causing their values to decline. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Partners Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

GPIM 57384

VIDEOS AND PODCASTS

Maria Giraldo, Investment Strategist for Guggenheim Investments, joins Asset TV’s Fixed Income Masterclass.

Matt Bush and Maria Giraldo join the Macro Markets podcast to discuss our newly published Quarterly Macro Themes for 1Q 2024.

Guggenheim Investments represents the investment management businesses of Guggenheim Partners, LLC ("Guggenheim"). Guggenheim Funds Distributors, LLC is an affiliate of Guggenheim.

Read a prospectus and summary prospectus (if available) carefully before investing. It contains the investment objective, risks charges, expenses and the other information, which should be considered carefully before investing. To obtain a prospectus and summary prospectus (if available) click here or call 800.820.0888.

Investing involves risk, including the possible loss of principal.

*Assets under management is as of 3.31.2024 and includes leverage of $14.5bn. Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, and GS GAMMA Advisors.

This is not an offer to sell nor a solicitation of an offer to buy the securities herein. GCIF 2019 and GCIF 2016 T are closed for new investments.

©

Guggenheim Investments. All rights reserved.

Research our firm with FINRA Broker Check.

• Not FDIC Insured • No Bank Guarantee • May Lose Value

This website is directed to and intended for use by citizens or residents of the United States of America only. The material provided on this website is not intended as a recommendation or as investment advice of any kind, including in connection with rollovers, transfers, and distributions. Such material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. All content has been provided for informational or educational purposes only and is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation. Investing involves risk, including the possible loss of principal.

By choosing an option below, the next time you return to the site, your home page will automatically

be set to this site. You can change your preference at any time.

We have saved your site preference as

Institutional Investors. To change this, update your

preferences.

United States Important Legal Information

By confirming below that you are an Institutional Investor, you will gain access to information on this website (the “Website”) that is intended exclusively for Institutional Investors and, as such, the information should not be relied upon by individual investors. This Website and any product, content, information, tools or services provided or available through the Website (collectively, the “Services”) are provided to Institutional Investors for informational purposes only and do not constitute a recommendation to buy or sell any security or fund interest. Nothing on the Website shall be considered a solicitation for the offering of any investment product or service to any person in any jurisdiction where such solicitation or offering may not lawfully be made. By accessing this Website, you expressly acknowledge and agree that the Website and the Services provided on or through the Website are provided on an as is/as available basis, and except as partnered by law, neither Guggenheim Investments and it parents, subsidiaries and affiliates nor any third party has any responsibility to maintain the website or the Services offered on or through the Website or to supply corrections or updates for the same. You understand that the information provided on this Website is not intended to provide, and should not be relied upon for, tax, legal, accounting or investment advice. You also agree that the terms provided herein with respect to the access and use of the Website are supplemental to and shall not void or modify the Terms of Use in effect for the Website. The information on this Website is solely intended for use by Institutional Investors as defined below: banks, savings and loan associations, insurance companies, and registered investment companies; registered investment advisers; individual investors and other entities with total assets of at least $50 million; governmental entities; employee benefit (retirement) plans, or multiple employee benefit plans offered to employees of the same employer, that in the aggregate have at least 100 participants, but does not include any participant of such plans; member firms or registered person of such a member; or person(s) acting solely on behalf of any such Institutional Investor.

By clicking the "I confirm" information link the user agrees that: “I have read the terms detailed and confirm that I am an Institutional Investor and that I wish to proceed.”