A version of this article appeared in Starling Trust’s 2023 Compendium.

In investing, risk has many faces, but all risks have one thing in common: uncertainty over the future course of events. Markets change, the economy evolves, policy responds, and exogenous shocks can come from anywhere. Most recently, markets were shocked by vulnerability in the banking sector, which itself was precipitated by extraordinary monetary easing in response to the pandemic, followed by aggressive monetary tightening in order to rein in runaway inflation. We don’t know where the next crisis will come from, but as an asset manager one of our responsibilities is to make sure our clients are best positioned to minimize risk and maximize return potential in good markets and bad.

For an organization to successfully meet complex and constantly changing risks and challenges, and take advantage of opportunities, it is critical to establish an operational structure and a management process that is capable of adjusting creatively and coherently—as a group. To try to meet this challenge, at Guggenheim Investments, we rely on a process built upon the bedrock of behavioral finance and designed to mitigate cognitive biases in making decisions. By deliberately disaggregating our decision-making process into teams of specialists who provide specific inputs to that process, we created a working system that shows behavioral science can deliver real-world solutions. The success of such a process requires an organizational discipline of collaboration and cooperation shared across the teams of specialists, and a common culture of communication and interdependency.

Looking Beyond the Agg

Successful investing in fixed income is no easy feat—bond selection is a process of elimination among millions of possible options rather than simply picking a winner. The proliferation of government bonds in the benchmark Bloomberg U.S. Aggregate Index (the Agg) means that the most compelling fixed-income investments lie beyond its limited scope. Identifying those takes a rigorous, disciplined investment decision-making process. We believe the integration of behavioral finance into our analyses—along with our ability to adhere to an investment process that we have designed to be predictable, scalable, and repeatable—is reflected in our performance.

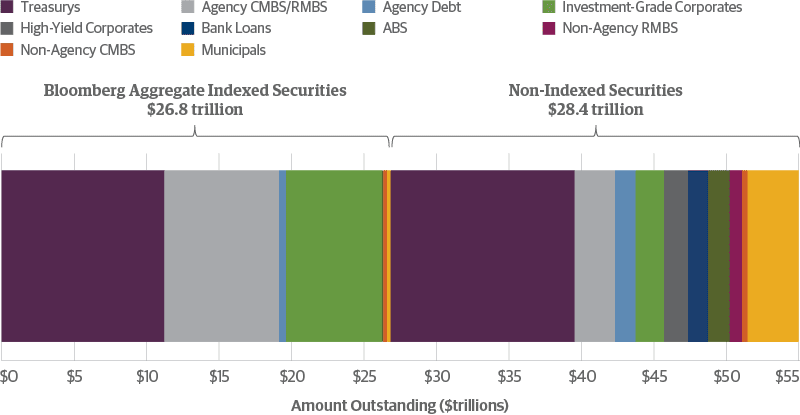

Since its creation in 1986, the Agg has been the most widely used proxy for the U.S. bond market. Inclusion in the Agg requires that securities be U.S. dollar-denominated, investment-grade rated, fixed rate, taxable, and have above a minimum par amount outstanding. In the early years of its existence, the Agg was a useful proxy for the fixed-income universe, which at the time primarily consisted of Treasury securities, Agency bonds, Agency mortgage-backed securities (MBS), and investment-grade corporate bonds—all of which met the foregoing inclusion criteria. However, the broad fixed-income universe has evolved significantly since then. Investors now have many more options to evaluate with the growth of sectors such as asset-backed securities (ABS), non-Agency residential MBS (RMBS), high-yield corporate bonds, leveraged loans, floating-rate bonds, and municipal bonds. Rather than reflecting the broader fixed-income market, with a market capitalization of $26.6 trillion, the Agg represents less than half of the investable universe, leaving out over $28 trillion of non-indexed securities.

The Bloomberg U.S. Aggregate Bond Index Represents Less than Half the Fixed-Income Universe

Source: Guggenheim Investments, SIFMA, S&P LCD, Bloomberg. Excludes sovereigns, supranationals, and covered bonds. Data as of 12.31.2022.

The Risk Mitigation Advantage of Active Management

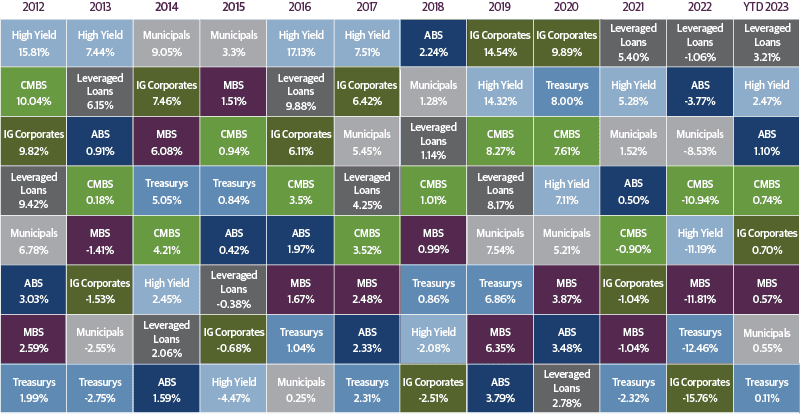

With the Agg so heavily concentrated in lower yielding and longer duration Treasury and Agency securities, while the broader fixed-income universe offers such a wide range of investment opportunities, the ability to invest outside the benchmark becomes a potential advantage. More importantly, the ability of active fixed-income managers to adjust their portfolio positioning as risks emerge and trading opportunities develop is not possible with a passive or index-constrained strategy. Of course, there will be periods when the Agg will outperform an active fixed-income manager, but we believe that, over a cycle, capable active managers should be able to find opportunity and avoid risk in the effort to achieve better results for their clients. The nearby chart of fixed-income returns, by sector index since 2012, demonstrates how different types of fixed income have performed.

Since 2012, an Agg component—Investment-Grade Corporates—has only topped the return list in two years, with the other years led by out-of-index sectors. A talented active fixed-income manager would hypothetically be able to trade in and out of the different sectors and allocate to the better performers every year. A passive strategy is limited to the weightings of the sectors contained in the Agg.

Asset Allocation Matters, Particularly in Today’s Volatile Environment

Sector Index Returns

Source: Guggenheim Investments, Bloomberg, Factset. Data as of 2.28.2023. Past performance does not guarantee future results. Performance will vary over different market cycles. Each asset class is represented by corresponding index: High Yield by Bloomberg U.S. Corporate High-Yield Index, Investment-Grade Corporates by Bloomberg U.S. Corporate Bond Index, Municipals by Bloomberg U.S. Municipal Bond Index, CMBS by Bloomberg U.S. CMBS Investment-Grade Index, Leveraged Loans by Credit Suisse Leveraged Loan Index, Treasurys by Bloomberg U.S. Treasury Index, MBS by Bloomberg U.S. MBS Index, ABS by ICE BofA U.S. Fixed & Floating Rate Asset Backed Securities Index. Index information is provided for illustrative purposes only and is not meant to represent the performance of the strategy or its underlying investments. Asset-backed securities (ABS), including mortgage-backed securities and CLOs, are complex investments and not suitable for all investors. Some ABS may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, including credit risk, interest rate risk, counterparty risk and prepayment risk. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

Unlike equity investing, where passive strategies have generally outperformed active managers, active fixed-income managers have generally outperformed passive strategies. Over the past 10 years, the average active large-cap equity fund manager has underperformed the benchmark index 78 percent of the time. In contrast, over the same 10-year period, the average active intermediate-term bond fund manager has outperformed the Agg 60 percent of the time.

Trailing One-Year Total Return Percentile Rank of Index Within Respective Morningstar Category

Source: Guggenheim Investments, Morningstar as of 3.31.2023. Past performance does not guarantee future results. Based on institutional share class. S&P 500 is compared against actively managed funds in the Morningstar U.S. Fund Large Blend Category. Bloomberg U.S. Aggregate Bond Index is compared against a combination of actively managed funds in the Morningstar U.S. Fund Intermediate Core Bond and Morningstar U.S. Fund Intermediate Core-Plus Bond categories. Each line represents the performance ranking percentile of a respective benchmark relative to the funds in the aforementioned categories. The best performance ranking percentile is 1 percent, and the worst performance ranking percentile is 100 percent. If the benchmark’s performance ranking is below 50 percent, then the majority of funds underperformed the benchmark (bottom half, unshaded). Conversely, if the benchmark’s performance is above 50 percent, then the majority of funds outperformed the benchmark (top half, shaded).

The different characteristics and market structure for stocks and bonds help account for different performance outcomes. The universe of listed stocks in the United States amounts to only about 3,000 companies, with a total market capitalization of approximately $44 trillion1. All public companies report their financial results according to GAAP rules, generally with quarterly frequency, and comply with fair disclosure rules. Moreover, publicly traded equities generally have exchange-based price discovery on a continuous basis. This relative homogeneity and transparency of financial data, news disclosures, and market data makes the equity market as close to an efficient market as it gets. The fixed-income universe, on the other hand, is sprawling, diverse, and huge, with approximately $55 trillion outstanding2. Unlike investment-grade corporates, Treasurys, and Agency securities, the non-indexed sectors of the fixed-income market—particularly structured credit and bank loans—have a wide range of structures, documentation, and reporting protocols. In addition, it is an over-the-counter market where pricing is less transparent. The complexity of the deal structures and security-specific collateral of certain securities—such as commercial ABS, CLOs, and bank loans—require proactive and comprehensive credit and legal analysis. It takes significant resources to take advantage of the opportunities in the non-indexed part of the market, which helps to explain why active management can realize the value of the inherent information premium, but passive management cannot*.

Decision Making Grounded in Behavioral Finance

We believe that one of the most important components of successful active management is an investment process that is designed to be repeatable, scalable, and predictable in all market conditions.

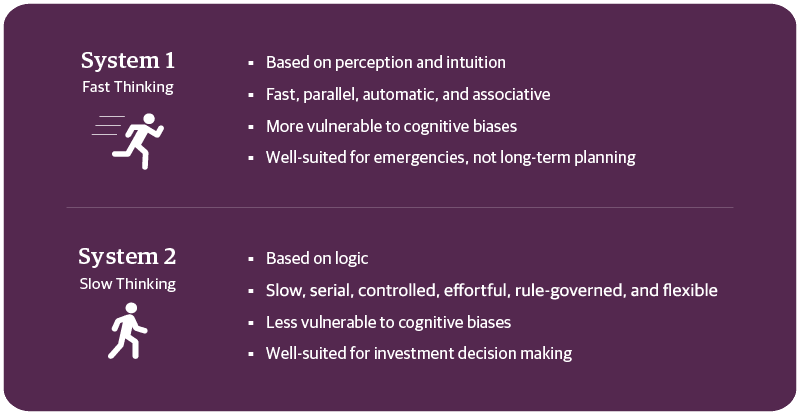

Decision making is an inherently flawed process. Oftentimes we think we are making a rational decision based on experience or intuition, but, as Nobel Prize winner Daniel Kahneman and his colleague Amos Tversky demonstrated, it is usually based on fundamentally incorrect logic caused by cognitive biases. Based on a series of groundbreaking experiments, Kahneman and Tversky used a metaphor of two systems of behavior that drive the way humans make decisions. System 1 behavior is automatic, rapid thinking, intuitive, and emotional. System 2 behavior is slower, deliberative, effortful, and logical.

Decision-Making Process

The human mind is capable of generating complex patterns and ideas while making Type 1 decisions, but these decisions are typically helped by shortcuts of intuitive thinking, or heuristics, that render us vulnerable to cognitive biases. These biases include anchoring (when a known value is considered before estimating an unknown quantity), representativeness (when judgements are rendered based on similarities between items without considering other factors) or availability (when assessing the probability of an event is judged by the ease with which similar occurrences can be brought to mind).

The biases inherent in System 1 behavior exist for organizations as well as individuals. Decisions at many investment firms are left in the hands of a star investor or a small group of portfolio managers who might be more vulnerable to bias risk. A far better approach is to try and produce System 2 behavior by slowing down decision making into an orderly series of steps and, in so doing, minimize cognitive biases and remove the emotional component from the process. We believe System 2 thinking potentially leads to superior long-term investment decisions. At Guggenheim Investments, we have embraced Kahneman and Tversky’s pioneering work in behavioral science and founded our entire investment process upon it.

Translating Behavioral Science into an Active Management Investment Process

To translate the lessons of behavioral finance into practice, we designed an investment process that seeks to mitigate cognitive biases so that our decisions are thoughtful and systematic rather than driven by impulse or emotion. To accomplish this, we disaggregate the investment process into its primary component functions, executed by four specialist groups: Macroeconomic and Investment Research, Sector Teams, Portfolio Construction, and Portfolio Management. By disaggregating the investment process in this way, we have made it purposefully difficult to fall into System 1 decision making. Investments are made only after taking input from all four groups.

The Macroeconomic and Investment Research Group provides the rest of the investment team with the outlook on the U.S. and global business cycle, market forecasts, and policy views. The Group establishes the house view on the labor market, inflation, productivity, and other drivers of economic growth, and evaluates debt and equity markets, as well as interest rates and commodities. Policy views encompass regulatory initiatives, fiscal policy, and monetary policy at the Federal Reserve and other global central banks.

The Sector Teams are responsible for sourcing and analyzing the most compelling risk-adjusted investments and providing ongoing risk monitoring. They take input from the macroeconomic team and provide security recommendations to portfolio managers, who decide on asset allocation. The Sector teams are the experts on their respective sectors: investment-grade and high-yield corporate bonds, bank loans, asset-backed securities, collateralized loan obligations, non-Agency residential mortgage-backed securities (MBS), commercial MBS, commercial real estate debt, municipal bonds, Agency MBS, and Treasury/Agency securities.

The Portfolio Construction Group provides strategy, research, and risk management analysis, and focuses on optimizing portfolio positioning for each client and fund by formulating model portfolios. The Portfolio Construction Group also conducts portfolio level risk analysis to evaluate whether the risk positioning is appropriate for each client.

The Portfolio Management team interacts with the Portfolio Construction Group, the Macroeconomic and Investment Research Group, and the Sector teams to make appropriate allocations for any given strategy. It synthesizes the collective work of the different groups to manage according to the investment guidelines of each client and fund. The Portfolio Management team is also the primary point of contact for clients for any updates and reporting that may be required to fulfill our client service obligations.

A major goal in the disaggregation of our process is to foster expertise in separate areas of investment decision making. In his seminal work The Wealth of Nations, Adam Smith observed that the division of labor in any enterprise increases productivity and leads to greater prosperity. There are several key benefits to the division of labor. First, each group becomes a specialist with specialized knowledge. Second, specialization enables each group to be more efficient with their time as they focus on their primary task. Last, specialization results in more innovation as each group pursues its task. Smith used the example of different levels of productivity for a farm worked by generalists versus a farm that employs specialists in each task.

Each of our individual investment professionals and their teams are fully aware of the purpose and intent of this structural design and the decision-making process. Adhering to the principles of behavioral finance is part of our corporate culture. The dynamism of this process is captured in the formal and informal interaction of our four specialized investment teams, and the constant communication within, between, and among the teams.

The Process is the Strategy

In his book, Team of Teams: New Rules of Engagement for a Complex World, General Stanley McChrystal explained that resilience and adaptability are critical to an organization’s ability to successfully contend with complex challenges. This is true whether these challenges are identified in advance or when they emerge unexpectedly, such as when Captain Sullenberger’s crew was forced to deal with the bird strike in their plane’s engines, or Boston area trauma centers had to manage the overwhelming rush of victims from the marathon bombing. As McChrystal said of these two teams, they succeeded because they were “capable of adjusting to the unexpected with creative solutions on the spot, coherently and as a group. Their structure—not their plan—was their strategy.”

We believe this is also true for asset management teams. Whether markets are moving quickly, as during the pandemic’s market volatility or the recent Silicon Valley Bank/Credit Suisse failures, or when they are less volatile, the same disciplined process is called upon to make investment decisions. Our actively managed fixed-income vehicles follow the same process. We believe the value of a practical application of behavioral science to our work has been borne out by our performance over time.

Important Notices and Disclosures

1. Source: SIFMA. Data as of 3.31.2023.

2. Source: SIFMA, S&P LCD, Bloomberg. Excludes sovereigns, supranationals, and covered bonds. Data as of 12.31.2022.

*There is no guarantee that an active manager’s views will produce the desired results or expected returns, which may lead to under-performance. Actively managed investments generally charge higher fees than passive strategies, which could affect performance. In addition, active and frequent trading that can accompany active management, also called “high turnover,” may lead to higher brokerage costs and have a negative impact on performance. Further, active and frequent trading may lead to adverse tax consequences.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward- looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC.

Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy or, nor liability for, decisions based on such information.

Investing involves risk, including the possible loss of principal. Investing in fixed-income instruments is subject to the possibility that interest rates could rise, causing their values to decline. Asset-backed securities (ABS), including mortgage-backed securities and collateralized loan obligations (CLOs), are complex investments and not suitable for all investors. Investors in ABS generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some ABS may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, including credit risk, interest rate risk, counterparty risk and prepayment risk. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Partners Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, GS GAMMA Advisors, LLC, and Guggenheim Partners India Management.

GPIM 57751

The Advantages of Investing in Infrastructure and Other Real Assets

Portfolio Management Outlook: Staying Focused Amid Geopolitical Uncertainty