The private debt asset class has grown in recent years as an increasing number of asset managers have launched dedicated commingled funds, founded business development companies, and raised separately managed accounts to meet investor demand.

This report discusses directly originated loans that are made to corporate borrowers. These loans are primarily cash flow based but may occasionally have an asset coverage component to them. These direct loans are often held by one or a handful of lenders as opposed to the broadly syndicated loan market, where there are typically dozens of holders of a single issuance.

Navigating this asset class can be daunting simply because of the sheer number of private debt managers marketing products and the lack of transparent data around the asset class. Guggenheim Investments has over 20 years of experience as an originator of and investor in private debt and is well-positioned to help investors pursue their investment objectives in the private debt market.

Report Highlights

- We believe the current environment for private debt offers the opportunity for compelling risk-adjusted returns in addition to attractive pricing, leverage, and documentation.

- Private debt has the potential to provide higher current income and returns than comparable below investment-grade fixed-income alternatives by taking advantage of the illiquidity premium, or the potential for excess return for investing in assets that cannot easily be converted into cash.

- The two pillars of successful private debt investing are sourcing and underwriting, both at closing and ongoing through monitoring.

- Guggenheim Investments (Guggenheim) has invested over $30 billion in over 550 middle market loans, and over this time have sought to originate direct loans with improved economics, relative credit strength, improved structural protections1, and enhanced control vs. liquid credit alternatives.

- Our private debt platform has historically generated a broad funnel of lending opportunities that can lead to differentiated portfolios of private debt assets, which are managed by our large, integrated investment team.

Introduction to Private Debt

The private debt asset class has experienced significant growth in recent years as an increasing number of asset managers have launched dedicated commingled funds, founded business development companies, and raised separately managed accounts. This growth has been fueled by investors that have recognized the potential for enhanced risk-adjusted return that private debt can bring to their portfolios relative to corporate bonds.

Private debt can include direct lending, real estate, infrastructure, mezzanine, venture, distressed, and asset-based lending. The focus of this report is on directly originated loans that are made to corporate borrowers. These loans are primarily cash flow based but may occasionally have an asset coverage component. These direct loans are often held by one or a handful of lenders as opposed to the syndicated loan market, where there are typically dozens of holders of a single issuance.

Direct lending has been present in some form for decades. Commercial banks and other local lenders used to dominate the market for loans to businesses that were too small to warrant financing from large institutional markets. As companies grew and their need for financing increased, banks provided additional debt capital, often by syndicating the debt to large institutional clients. And as banks’ business models evolved, generating fees through the syndication of debt became much more lucrative than holding loans on their balance sheets.

The increased capital formation that private debt has experienced has left some to worry about the market being overheated. In reality private equity capital formation has far surpassed that of private debt, and private equity remains the most significant driver in private credit deal activity. In addition, the increase of capital flowing to private debt managers has increased the opportunity set that private debt lenders can address, as transactions that were once too large can now become achievable. Furthermore, while there have been new entrants on the smaller end of the market, the upper end of the market has not added many (if any) new players, despite experiencing considerable growth in assets under management.

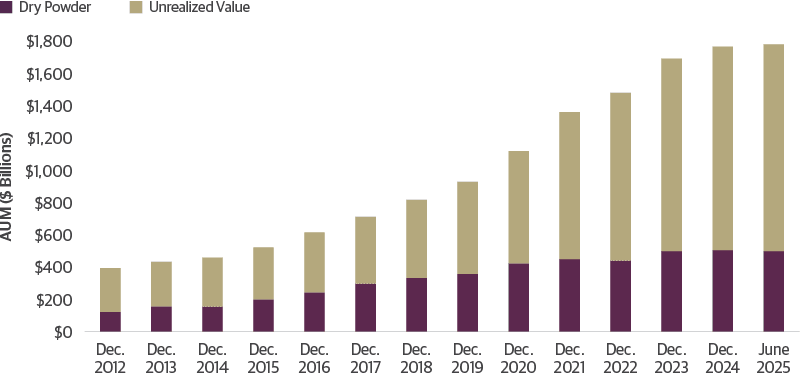

Total Global Private Debt Exceeds $1.7 Trillion

Source: Guggenheim Investments, Preqin, Federal Reserve. Data as of 6.30.2025. Note: Dry Powder refers to committed but not invested capital. Invested capital is committed and invested capital (typically in the form of loans). Assets under management (AUM) is the sum of invested capital and dry powder. AUM data reported with a six-month lag.

The so-called middle market of corporate borrowers is a broad category that encompasses businesses in every industry in the United States. The middle market has grown significantly over the last decade in two ways: a growing economy has created more businesses that have grown into substantial enterprises, and the breadth of the market has expanded as private equity and private debt providers have grown in scale to compete with the public equity and debt markets for transactions. According to the National Center for the Middle Market, the U.S. middle market represents over 200,000 businesses that combined would count as the world’s third largest economy. Nearly one third of all jobs and private sector gross domestic product are encompassed by the middle market. This subsection of the economy includes businesses with revenues of $10 million to $1 billion. We specialize in middle market loans typically ranging in size from $100–$500 million for borrowers with earnings before interest, taxes, depreciation, and amortization (EBITDA) of $20–$250 million.

In times of market volatility, banks have historically pulled back on lending, leaving a significant funding gap in the middle market. We witnessed this phenomenon during the banking crisis of March 2023, but longer-term trends emanate from Russian aggression in Ukraine, and still linger from the onset of the COVID crisis in March 2020. More recently, we witnessed this dynamic in 2025 amid lower-than-expected M&A volumes and concerns around Tariffs and fiscal policy uncertainty. As in past periods of market volatility, we believe the current environment for private debt offers the opportunity for compelling risk-adjusted returns in addition to attractive pricing, leverage, and documentation.

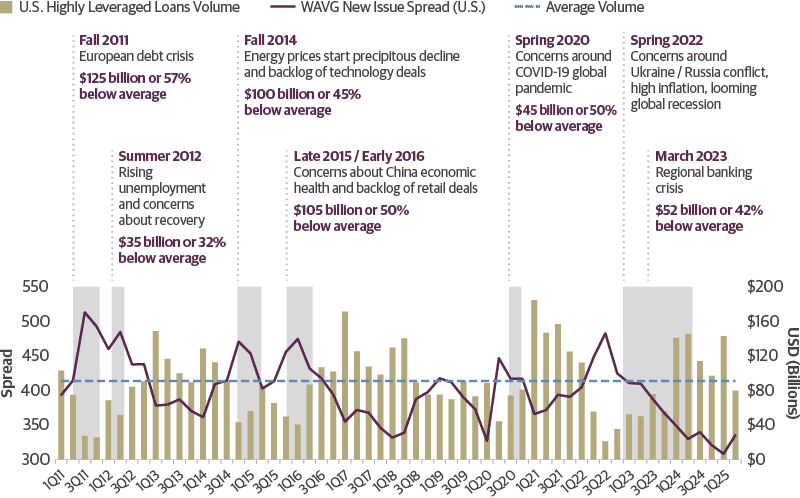

Banks Pull Back in Volatile Times, Expanding Private Debt Lending Opportunities

Total Volume and Weighted Average Spread for New Issue Loans

In times of market volatility, banks have made loans harder to get and more expensive, leaving a significant funding gap for the middle market.

Total Volume and Weighted Average Spread for New Issue Loans

Source: Guggenheim Investments, S&P LCD. Data as of 6.30.2025. Historical trends may not continue. Guggenheim Investment’s market characterization is based on subjective determinations that it believes are reasonable but other investors may disagree with such characterization. Data reflects the U.S. broadly syndicated leveraged loans market, as tracked by Pitchbook. The dataset includes all leveraged loans syndicated in the U.S., including USD-denominated tranches of borrowers domiciled in Europe and other locations.

The Return Profile of Private Debt

Private debt has the potential to provide higher current income and returns than comparable below investment-grade fixed-income alternatives through taking advantage of the illiquidity premium, or the potential for excess return for investing in assets that cannot easily be converted into cash. Direct lending can potentially add 100–500-plus basis points of additional yield to the traditional syndicated market (and higher depending on the amount of leverage used by the vehicle or if the manager is investing in subordinated debt and junior capital) with the ability to negotiate better structural protections than broadly syndicated loans.

The primary return driver for private debt is interest income, although additional drivers of return may include origination fees, transaction fees, prepayment fees, and equity investments and/or warrants. Negative drivers of returns are default and recovery rates, typically condensed into a single statistic of loss rate.

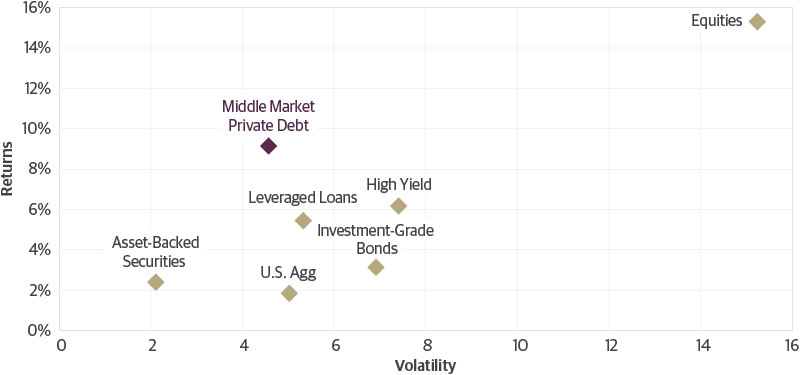

Comparing Risk and Return Across Select Asset Classes

Q3 2015 through Q3 2025 Annualized

Source: Guggenheim Investments, Bloomberg, Cliffwater, Morningstar. Data as of 9.30.2025. Past performance does not guarantee future results. Performance will vary over different market cycles. Each asset class is represented by the following corresponding index: Middle Market Private Debt: Cliffwater Direct Lending Index; equities: S&P 500; high yield bonds: Bloomberg U.S. High Yield Bond Index; leveraged loans: Morningstar LSTA U.S. Leveraged Loan Index; broad bond market benchmark: Bloomberg U.S. Aggregate Bond Index; investment-grade corporate bonds: Bloomberg U.S. Corporate Bond Index; asset-backed securities: Bloomberg U.S. Aggregate ABS Index.

Types of Private Debt Investment Vehicles

Investors in the asset class have coalesced around a few main investment vehicles for gaining exposure to direct lending. Common characteristics for each are as follows:

1. Commingled private debt funds

- Dedicated personnel with experience sourcing and underwriting private loans

- Fixed investment period typically ranging from one to five years with long hold periods

- Fund life of four to eight years or more

- “Evergreen” funds, which are not limited by investment size or maturity date, provide a similar investment profile without some of the restrictions of more traditional commingled private debt funds

2. Business Development Companies (BDCs)

- Registered investment vehicles that can be either private or publicly traded and can use up to 2:1 leverage

- Public BDCs may offer liquidity to investors through the sale of equity in the public market, but are prone to market volatility

- Private BDCs typically have longer lock up period of five years

3. Middle market collateralized loan obligations (CLOs)

- Issued by private debt managers or large credit platforms

- Typically less liquid than syndicated loan CLOs given smaller size of the issuances and illiquid nature of the underlying assets

4. Separately managed accounts (SMAs)

- Often offered in conjunction with, or in lieu of, commitments to commingled funds or BDCs

- Larger capital allocators may have the ability to create a SMA with a manager in order to build customized parameters for investing in the asset class

5. Small Business Investment Company (SBIC)

- Regulated investment vehicle under the Small Business Administration intended to finance small businesses

- Managers will often build out a SBIC portfolio and then roll assets into BDC structure, allowing the fund to grow above SBIC cap

Each of these components is affected by what is happening in the syndicated market. Pricing (the interest rate associated with a loan) has historically been a function of a spread over syndicated loan market pricing, which can fluctuate based on market and economic conditions. When the syndicated loan market is active, borrowers have more options, which can lead to price compression. In times of weak demand, increasing upfront fees is one way for the loan market to find lenders, whereas when the loan market is strong, fees are often reduced to almost nothing. To the extent a lender can work directly with a borrower, the direct lender can capture the upfront fees and increase return.

The final component to returns is the loss rate, which is the product of the default rate x (1 – recovery rate). Based on our observations in investing in private debt, we generally expect that over long periods of time, default rates in private debt have shown to been similar to those of single-B rated leveraged loans.

That leaves the recovery rate of principal and interest in the event of a default on the loan, which can be a key differentiating factor in producing attractive returns in a private debt portfolio. We believe that the two most critical factors in driving strong recoveries are: owning the majority of the debt in the debt capital stack (thereby being the likely fulcrum security that will drive or control a restructuring), and having some combination of financial maintenance covenants, limitations on future indebtedness, enhanced collateral protections, and appropriate EBITDA definitions, which allow us to catch potential credit deterioration and use the aforementioned control to push the company to either reduce risk or increase economics in order to compensate for higher risk.

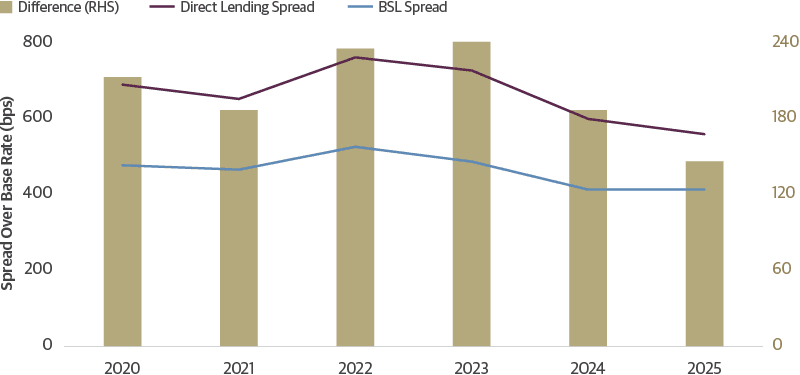

Private Credit Spreads Appear Attractive Relative to Leveraged Loans

Source: Guggenheim Investments, Pitchbook. Data as of 12.31.2025. Direct lending spread data reflects senior secured first-lien loans and unitranche facilities. BSL data reflects loans issued to borrowers rated B-.

The Use of Leverage in Private Debt

The use of leverage in private debt vehicles can be controversial given the impact that leverage can have on returns in the asset class and the added risk it creates. Many private debt investment vehicles have turned to leverage as a way to compensate for declining loan spreads as the funds look to maintain a consistent absolute return. The more leverage that is employed in a fund, the greater the volatility of potential returns to the investor.

Key Terminology

Terminology used to explain loans’ structure includes:

Senior Loans

- First lien secured loans that will closely mimic syndicated bank loan structures and offer a smaller illiquidity premium

- Offerings can also include revolvers, which are more difficult for direct lenders because they require some form of cash collateralization without offering significant current income

Unitranche

- Combines senior and junior capital into a single loan

- Deeper in capital structure than senior loans

- Also referred to as “stretch senior”

- Borrowers like this structure because they deal with a single lender, making it easier to handle acquisitions, amendments, etc.

First Out/Last Out

- Highly structured loans where lenders will tranche out a unitranche loan after it closes

- First out will often be sold to lender with lower cost of capital (banks or other highly rated financial institutions) looking for lower risk investments

- Private debt funds will keep last out, which has higher yield than the overall structure

- Agreement Among Lenders outlines priority of payments and rights and remedies

- Less utilized today due to the prevalence of leverage facilities

Second Liens

- Secured debt behind senior bank debt

- Structures often mimic the syndicated bank loan market where second liens offer small amount of additional leverage behind a much larger first lien loan

Mezzanine

- Junior, unsecured capital often behind several turns of senior bank debt

- Typically fixed rate, occasionally with equity co-investment component

- Declined in popularity since the GFC as more direct lenders enter the space and offer unitranche or higher senior leverage

Attachment Point

- Place in capital structure through which a debt investment is levered. A second lien loan that represents 1.5x of leverage and sits behind 4x of senior debt would attach at points 4x–5.5x

Loan to Value (LTV)

- Percentage of enterprise value through which debt investment represents. A 4x senior loan on a 10x Enterprise Value business would be at a 40 percent LTV. A second lien that represents 1.5x turns of leverage on the same business would be at a 55 percent LTV

Fund vehicles like BDCs and SBICs have leverage levels capped based on regulatory restrictions. For BDCs, that amount is 2:1, while for SBICs it is also 2:1, but with no restrictions on the underlying composition of the assets (e.g. lien, security, covenants, etc.). During the Global Financial Crisis (GFC), a number of BDCs and SBICs ran into trouble due to the high amount of leverage they were utilizing because of markdowns on the asset values in their portfolios (despite BDC leverage being capped at 1:1 during this time). Some were forced to shut down while others sold their assets at a discount to managers who had been more prudent in their underwriting and use of leverage.

Leverage is a useful tool, but we do not believe that leverage should drive portfolio construction. Instead, it should act simply as an enabler of the portfolio to meet the investment objectives of the investor. We believe leverage should be employed conservatively and only in instances when it can provide investors with greater flexibility and optionality. For example, the use of leverage may allow a fund to broaden its investable universe by investing in less risky but lower yielding assets while meeting its target return.

The Keys to Successful Investing in Private Debt

We believe two key pillars of successful private debt investing are sourcing and underwriting (both at closing and ongoing through monitoring). These two activities can vary in importance over the course of the credit cycle. As finding private debt investments gets more difficult and sourcing increases in prominence, underwriting standards can weaken with competition and with the expectation that a benign credit environment will continue. However, as the credit cycle turns and pressure mounts on weaker borrowers, underwriting will show itself to be the determining factor in driving returns in the asset class.

Sourcing private debt investments is typically broken out into two categories: sponsored and non-sponsored. Sponsored transactions are done in partnership with a private equity firm, financing a leveraged buyout, growth equity investment, or dividend recapitalization. Non-sponsored transactions can vary in size and sophistication from a family business with no audits and a few million dollars in revenue to a public company with a several hundred million dollar market capitalization. The common theme in these transactions is that the borrower is typically not a sophisticated financial investor. Non-sponsored transactions can often be more complex due to lack of transparent financials and can take longer to execute on as borrowers may not have a pressing need for capital. The rewards can be significant, however, as non-sponsored transactions typically come with higher pricing, better structural protections1, and greater incumbency value.

The underwriting process will vary depending on whether a transaction is sponsored or non-sponsored and by the type of investor. But most private debt managers have a similar process where teams are staffed with deal leads who run diligence and negotiate documentation and are supported by junior analysts who focus on due diligence efforts. Potential deals are presented to an investment committee comprising senior team members and a decision is made on whether to invest.

The Guggenheim Difference

For more than 20 years, Guggenheim Investments has invested over $30 billion in over 550 middle market loans, and over this time have sought to originate direct loans with improved economics, relative credit strength, improved structural protections1, and enhanced control vs. liquid credit alternatives. Since we began investing in private debt, Guggenheim Investments has had a consistent market presence with a selective approach, and our sourcing capabilities, underwriting expertise, and size allow us to be disciplined and patient but also drive outcomes through responsiveness and negotiation. The significant size of our capital base and our large team of 50 analysts covering the United States and Europe enable us to be important partners for potential borrowers, while the pace of fundraising and the size of our client base allow us the ability to be more selective in our investments relative to other market participants.

As with all our investments, we manage private debt sourcing and investment according to our investment process, which incorporates an integrated team approach to investing across the capital structure, with rigorous bottom-up credit research, deep industry expertise, and strong valuation conviction. Any investment or loan is subject to extensive due diligence, which includes a thorough exploration of any contracts or covenants by our specialized legal team of five internal lawyers.

Investment or loan decisions are not executed without unanimous approval by our Investment Committee, and positions and portfolios are monitored daily to assess whether any of the factors that led to the allocation of capital have changed.

Our private debt platform has historically generated a broad funnel of lending opportunities that can lead to differentiated portfolios of middle market private debt assets, which are managed by our large, integrated investment team along with more than 10 dedicated origination professionals. Our significant investment in resources allows us to be active in both sponsored and non-sponsored transactions. Overall, over 100 professionals are involved in the direct lending process, and we currently have over 1,500 issuers across our platform.

We have dedicated sourcing and underwriting teams in both the United States and Europe, with investment decisions approved by a central Investment Committee. With $12 billion of direct lending assets across our platform, we are an important partner for private equity firms, deal brokers, and investment banks across these geographies, and are well-positioned to help private debt investors pursue their objectives.

Important Notices and Disclosures

1. Structural protections generally refer to mechanics negotiated into a loan document that can include but are not limited to covenants, security/collateral, obligor reporting requirements/lender information rights, etc. Protections neither assures a profit nor eliminates the risk of experiencing investment losses.

Past performance is not indicative of future returns

Investing involves risk, including the possible loss of principal. In general, the value of a fixed-income security falls when interest rates rise and rises when interest rates fall. The private debt assets and strategies discussed herein are not suitable for all investors. An investment in private debt assets is speculative and involves a high degree of risk. No investor in a private debt strategy should have any need for any monies invested in the strategy to meet current needs or ongoing financial requirements and an investment in the strategy should only be made after consultation with independent qualified sources of investment and tax advice. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate. Exposure to high yield assets can subject an investment to greater volatility. Some assets may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices very volatile and they are subject to liquidity risk. There often in no secondary market for an investor’s interest in private debt assets and one is not expected to develop. A conflict of interest will often arise when Guggenheim or any of its affiliates participate in loan arrangements for which it is providing investment management services, investment banking services or other transaction related services and in which the strategy also invests.

©2026, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.

67774

Portfolio Management Outlook: Sound Credit Fundamentals and Elevated Yields to Weather Tail Risks to Our Outlook

The Advantages of Investing in Infrastructure and Other Real Assets