This Macroeconomic Outlook report is excerpted from the First Quarter 2026 Fixed-Income Sector Views.

In 2026, we expect the U.S. economy to show solid real GDP growth a bit above 2 percent, while inflation is expected to resume its cooling trend. The third-quarter real GDP reading revealed positive underlying growth momentum, highlighting two primary drivers: robust consumer spending—benefiting from the wealth effect of rising asset prices—and a continued boost from AI investment.

In the first half of 2026, the expansion should be further supported by a rebound following the government shutdown, additional fiscal stimulus and support from monetary and financial conditions. This strong growth impulse is likely to moderate in the second half as fiscal stimulus fades, allowing the economy to move toward equilibrium.

Looking ahead, we expect growth to stabilize at around 1.7 percent in 2025 and maintain a similar pace in 2026, supported by fiscal measures under the One Big Beautiful Bill Act (OBBBA), which includes retroactive tax cuts that should lift personal tax refunds and provisions to broaden business investment. AI optimism and elevated asset prices are likely to sustain high-income household consumption, though the economy remains bifurcated. Housing and lower income households continue to face challenges, with depressed home sales, subdued housing investment, and rising credit card and student loan delinquencies.

The labor market remains a downside risk to our outlook, but conditions are cooling only gradually. Private sector payroll growth slowed from a three-month average of 203,000 in January 2025 to 29,000 in December, with gains highly concentrated in healthcare. The unemployment rate trended up since last summer, indicating that slower job growth reflects lower labor demand, not just slowing labor force growth. Fortunately, jobless claims remain low, and business sector financial health remains solid, with limited pressure on profit margins that typically precedes a wave of layoffs. We expect conditions to stabilize in 2026 as growth improves, while remaining attentive to the risk of a sharper deterioration that could weigh on consumer spending.

We expect core inflation to remain sticky over the next few months as gradual tariff passthrough continues. However, the bigger story for 2026 is likely to be one of fundamental inflation drivers resuming their downward trend. Leading measures of rent inflation continue to soften, which should lead to further downside for this large category of the inflation basket. And the softer labor market means wage pressures are easing, which should ease services inflation. We expect year-over-year core personal consumption expenditures inflation to fall to around 2.5 percent by the fourth quarter of 2026, with monthly readings somewhat closer to the Fed’s 2 percent target.

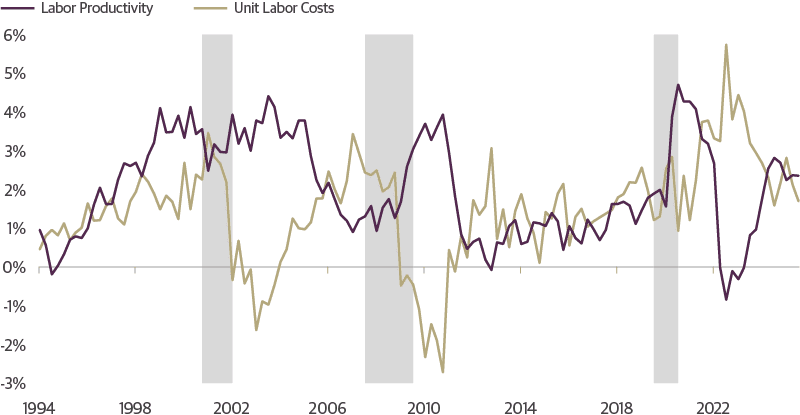

The outlook for solid growth, a stable labor market, and gradual disinflation reflects productivity growth that is expected to be relatively strong, reflecting the trend of recent years and some nascent gains from AI adoption in 2026. The Fed’s latest Summary of Economic Projections also reflects supply side optimism, with most participants seeing strong growth and lower inflation. Despite this, views on the path for monetary policy remain dispersed, reflecting different perspectives on neutral rates and the balance of risks to the Fed’s dual mandate. As the disinflationary trend becomes more apparent later in the year, we see the Fed easing to a neutral rate of 3–3.25 percent.

Solid Productivity Growth Should Help Sustain Growth and Ease Inflation

Labor Productivity, 8Q Annualized Change

Source: Guggenheim Investments, Haver Analytics. Data as of 6.30.2025. Gray areas represent recession.

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the authors, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward-looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

Investing involves risk, including the possible loss of principal. In general, the value of a fixed-income security falls when interest rates rise and rises when interest rates fall. Longer term bonds are more sensitive to interest rate changes and subject to greater volatility than those with shorter maturities. During periods of declining rates, the interest rates on floating rate securities generally reset downward and their value is unlikely to rise to the same extent as comparable fixed rate securities. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

Guggenheim Investments represents the following affiliated investment management businesses of Guggenheim Partners, LLC: Guggenheim Partners Investment Management, LLC, Security Investors, LLC, Guggenheim Funds Distributors, LLC, Guggenheim Funds Investment Advisors, LLC, Guggenheim Corporate Funding, LLC, Guggenheim Wealth Solutions, LLC, Guggenheim Private Investments, LLC, Guggenheim Investments Loan Advisors, LLC, Guggenheim Partners Europe Limited, Guggenheim Partners Japan Limited, and GS GAMMA Advisors, LLC. Not FDIC insured. Not bank guaranteed. May lose value.

GPIM 67411