Report Highlights

- Turning points in the monetary policy cycle provide a window of opportunity for strategic portfolio allocation decisions.

- History shows that when the economy is strong and the Federal Reserve (Fed) is hiking, risky assets have outperformed; when the Fed is paused and easing, longer duration higher quality fixed income has outperformed.

- Today we are in the middle of a pause phase, with rate cuts likely to follow when the Fed deems inflation at an acceptable level.

- This policy turning point offers investors the opportunity to increase allocations to strategies invested in higher quality fixed income and out of riskier assets like stocks as well as money market instruments.

- Historically, the Bloomberg U.S. Aggregate Bond Index (the Agg) outperformed money market instruments over the last three months of the Fed pause and through the easing cycle by a cumulative 5 percentage points on average.

- A strategy that outperformed the Agg would have performed even better against money markets.

- With the demonstrated record of outperformance by higher quality fixed income in the final months of a pause and over the easing phase of the policy cycle, we believe investors should consider adjusting allocations accordingly, particularly with money market fund assets at an all-time high of $6.1 trillion and bond prices significantly lower now than in past easing cycles.

Relative Performance at Policy Turning Points

History shows that monetary policy drives investment performance. When the Fed hikes or cuts the fed funds target rate in response to economic conditions—or stays on hold while it assesses the data—performance will differ by sector. There are certain times during the policy cycle when the expected performance differences can be quite stark: These turning points can provide a window of opportunity for strategic asset allocation decisions.

When the economy is starting to overheat and the Fed responds by raising the fed funds target rate, risky assets like stocks and below-investment grade credit tend to perform best. Conversely, when the Fed is cutting rates to address a slowing economy, longer duration higher quality bonds tend to outperform. Most sectors perform well when the Fed is neither hiking nor easing but on pause and considering its next move.

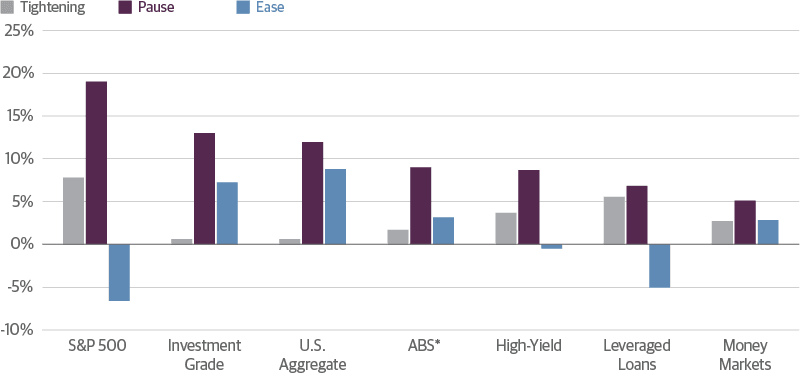

Higher Quality Fixed Income Has Outperformed When the Fed Is Easing

Asset class performance over the past five Fed monetary policy cycles.

Past performance does not guarantee future results. Source: Guggenheim Investments, Bloomberg. S&P 500: S&P 500 Total Return Index. Investment Grade: Bloomberg U.S. Corporate Total Return Value Unhedged USD. U.S. Aggregate: Bloomberg US Agg Total Return Value Unhedged USD. ABS: Bloomberg U.S. Agg ABS Total Return Value Unhedged USD. High Yield: Bloomberg U.S. Corporate High Yield Total Return Index Value Unhedged USD. Leveraged Loans: Credit Suisse Leveraged Total Return Index. Money Markets: Bloomberg U.S. Tr Bills: 1–3 Months TR Index Value Unhedged USD. Average Monthly Returns, Annualized. Data from February 1993 to July 2023. *Fixed rate.

During the pause phase, risky assets tend to outperform initially but eventually lose ground to higher quality fixed income as it becomes increasingly apparent that the economy is losing steam and rate cuts are coming. Historically, higher quality fixed income has outperformed over the combined pausing and easing part of the cycle.

The Current Policy Cycle Is at a Turning Point

Today we find ourselves near the end of a pausing phase in monetary policy execution. The Fed last hiked at the July 2023 Federal Open Market Committee (FOMC) meeting and has stayed on hold since then. While the economy has proven resilient in many ways, the lagged effects of 525 basis points of hikes are still impacting the economy. Stubbornly strong economic activity and inflation data have caused the Fed to pause plans to start cutting rates, but in our view policy tightening is having an effect.

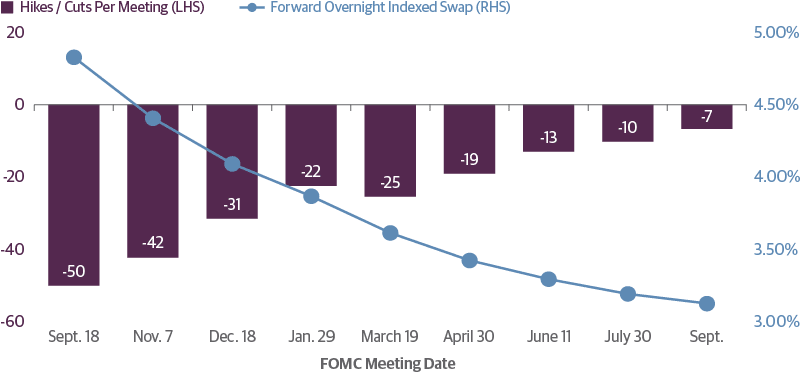

The Next Big Move for the Fed Will Be Rate Cuts

The Next Big Move for the Fed Will Be Rate Cuts

Source: Guggenheim Investments, Bloomberg. Data as of 8.5.2024.

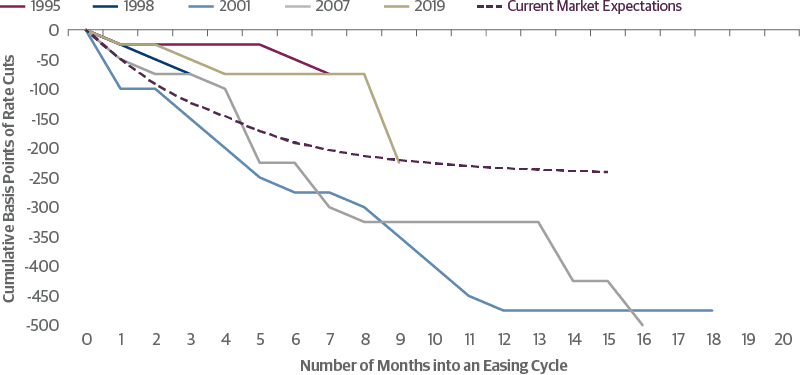

We believe the Fed will eventually cut more than the market is expecting. For comparison, the cumulative amount of easing in recent cycles has ranged from 75 basis points (1995 and 1998) to 550 basis points (early 2000s). The average amount of cuts for recent easing cycles was 285 basis points.

The Market Expects Fewer Rate Cuts than Normal in the Next Easing Cycle

Source: Guggenheim Investments, Bloomberg. Data as of 8.5.2024.

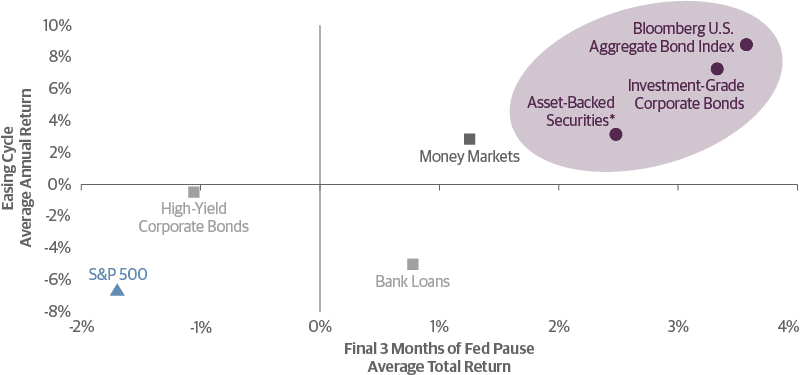

Higher Quality Fixed Income Outperformed Other Sectors, Including Money Markets

As the Fed nears the end of the pause phase of the cycle and starts easing, historical data show that higher quality fixed income outperformed riskier assets like stocks, as well as money market instruments. It is worth noting that in the last five easing cycles1, the 10-year Treasury yield has fallen by 147 basis points in the first 18 months on average after the Fed stops hiking rates.

Higher Quality Fixed Income Outperformed Risky Assets (and Money Markets) Leading Up to and During the Last Five Easing Cycles

Past performance does not guarantee future results. Source: Guggenheim Investments FactSet, Morningstar. Data as of 12.28.2023. Investment Grade Corporates: Bloomberg U.S. Corporate Bond Index. Asset-Backed Securities: Bloomberg U.S. Agg ABS Total Return Value Unhedged USD. High Yield: Bloomberg U.S. Corporate High Yield Bond Index. Bank Loans: Credit Suisse Leveraged Loan Index. Money Markets: Bloomberg U.S. Tr Bills 1-3 Months TR Index Value Unhedged. Average Monthly Returns, Annualized. Data from 1993 to July 2023. *Fixed rate.

For much of the past two years, the opportunity cost of moving into money markets has been low. While the Fed was aggressively hiking, anything with price sensitivity to changing interest rates or duration suffered. By definition, money markets do not have duration, and the Fed’s rate-hike campaign has increased yields on money market instruments to over 5 percent.

Money market instruments are high quality, very liquid investments, appropriate to have cash on hand to meet short-term goals, but for those with longer-term investment time horizons, with policy easing on the horizon, we believe the opportunity cost of not switching to higher quality fixed income will rise. As the following chart shows, the Agg has outperformed money market instruments by an average of approximately 500 basis points over the end of a pause and ensuing 12 months of the last five easing cycles. Naturally, a strategy that outperformed the Agg would have performed even better against money markets.

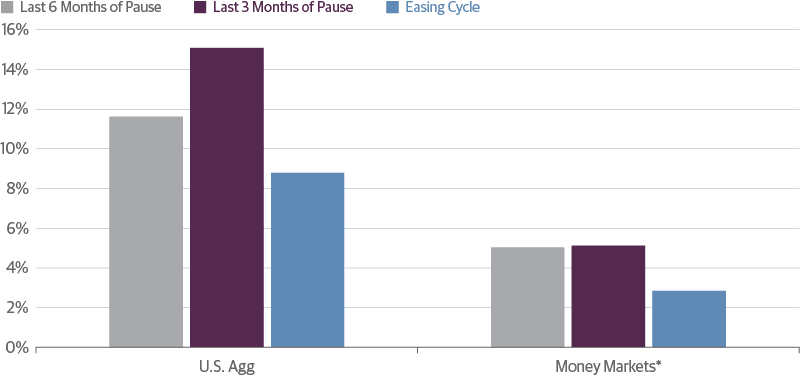

Track Record Favors the Agg over Money Markets at This Point in the Cycle

Past performance does not guarantee future results. Source: Guggenheim Investments, Bloomberg. Data as of 12.28.2023. Money market – Bloomberg Treasury Bill 1-3 Month Index.

Another view of this analysis shows the total average annualized returns to higher quality fixed income and to money markets over the most recent policy cycles. The last three months prior to the start of easing generated the highest relative outperformance for the Agg.

Money Markets Underperformed Three and Six months Before the First Cut

Past performance does not guarantee future results. Source: Guggenheim Investments, Bloomberg. Average Monthly Returns, Annualized. Data from 1993 to July 2023. Data as of 12.28.2023. Money market – Bloomberg Treasury Bill 1-3 Month Index.

Technical Considerations Related to Timing

While the window of opportunity to reallocate out of money market funds and into higher quality fixed income is open, there are two technical factors that suggest the window opening may narrow.

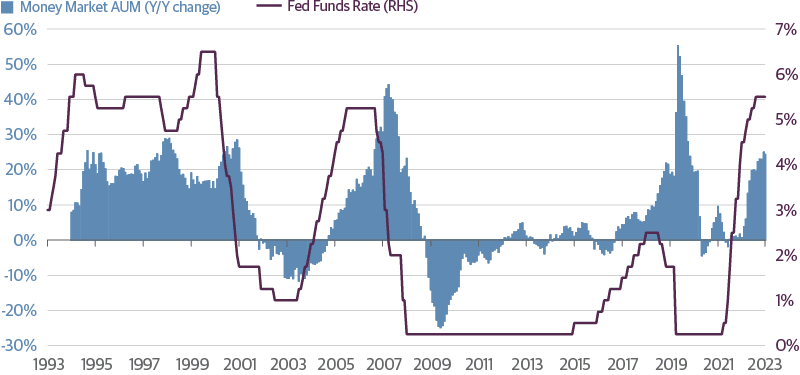

The first factor relates to the wall of money that typically follows changes in the fed funds rate on the way up and the way down. Since the Fed started hiking rates in March 2022, money market assets have risen 28 percent, or approximately $1.3 trillion, from $4.6 trillion to an all-time high of over $6.1 trillion. As cash leaves money markets—with a lag—when the Fed starts cutting rates, it can go into different investment opportunities, but bonds will likely be a beneficiary. Investors may be well-served to get ahead of that “money in motion.”

Money Market Fund Assets Move Based on Monetary Policy

Source: Guggenheim Investments, Bloomberg, ICI. Data as of 12.20.2023.

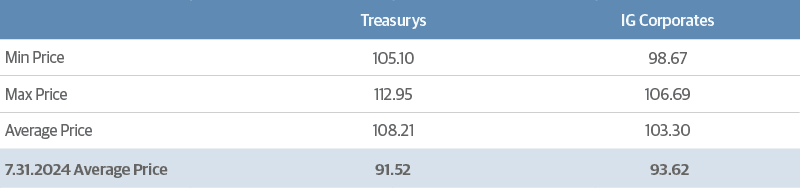

The second technical factor related to timing is dollar prices available in the market. As every bond investor knows, the historic size and pace of the 2022–23 rate-hiking regime brought down bond values significantly. The spike in rates has also kept many new issuers on the sidelines, and the reduced levels of par issuance has kept market dollar prices at much lower levels than they were heading into prior easing cycles. The lower average dollar price of bonds today suggests that in this easing cycle there may be a greater potential for price appreciation—also known as positive convexity—than in prior easing cycles. As more money moves into bonds and yields fall, these dollar prices typically rise.

Today’s Bond Prices, Lower Than in Prior Cycles, Present Price Appreciation Opportunity

Index dollar prices one month before easing cycles

Past performance does not guarantee future results. Source: Guggenheim Investments, BAML, Bloomberg, ICE BofA US Treasury Index, ICE BofA US Corporate Index. Data as of 7.31.2024. *Data does not include the current pause since it is unknown when it will end.

Investment Implications

The historical performance of various asset classes shows a pattern of outcomes tied to the phases of a monetary policy cycle. As the Fed comes to the end of the pause phase of the cycle and starts easing, historical data show that higher quality fixed income has outperformed riskier assets like stocks, as well as money markets. Alert investors considering when to reallocate into bonds will also want to consider technical factors that could affect the timing of such a move, including getting ahead of possible outflows from money market instruments and taking advantage of low dollar prices available in the market.

Research and analysis provided by Chris Squillante, Investment Strategist, Macroeconomic Research and Market Strategy Group.

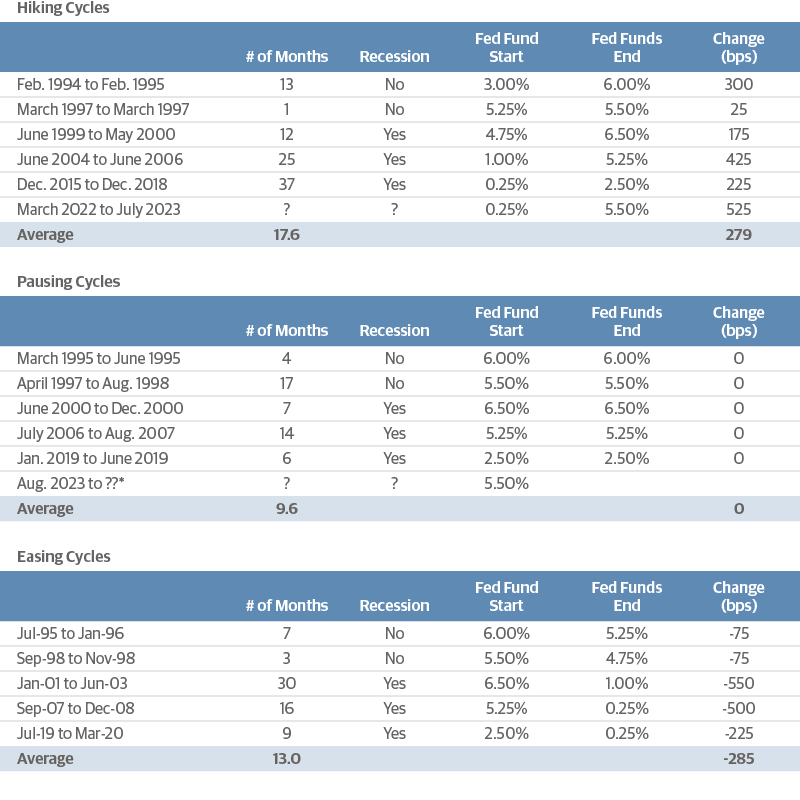

1. The analysis of performance during economic policy cycles is based on the following instances of Federal Reserve hiking, pausing, and easing:

Instances of Federal Reserve Hiking, Pausing, and Easing

*Data does not include the current pause since it is unknown when it will end

Important Notices and Disclosures

Investing involves risk, including the possible loss of principal. Investments in fixed-income instruments are subject to interest rate risk. In general, the value of a fixed-income security falls when interest rates rise and rises when interest rates fall. Longer term bonds are more sensitive to interest rate changes and subject to greater volatility than those with shorter maturities. During periods of declining rates, because the interest rates on floating rate securities generally reset downward, their market value is unlikely to rise to the same extent as the value of comparable fixed rate securities. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate.

One basis point is equal to 0.01 percent.

Bloomberg U.S. Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by U.S. and non-U.S. industrial, utility and financial issuers. Bloomberg U.S. Corporate High Yield Bond Index measures the USD-denominated non-investment grade, fixed-rate, taxable corporate bonds. Securities are classified as high yield if the middle rating of Moody’s, Fitch, and S&P is Bal/BB+/BB+ or below. The index excludes emerging market debt. Credit Suisse Leveraged Loan Index is designed to mirror the investable universe of the U.S. dollar-denominated leveraged loan market. S&P 500 Index is a capitalization weighted index of 500 stocks, actively traded in the U.S, designed to measure the performance of the broad economy, representing all major industries. Bloomberg U.S. Treasury Bill 1-3 Month Index tracks the market for treasury bills with 1 to less than 3 months to maturity issued by the U.S. government. Bloomberg U.S. Asset-Backed Securities Index is the ABS component of the Bloomberg U.S. Aggregate Bond Index, a flagship measure of the U.S. investment grade, fixed-rate bond market. The ABS index has three subsectors: credit and credit cards, autos and utility. Bloomberg U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar denominated, fixed-rate taxable bond market, including Treasurys, government-related and corporate securities, MBS Agency fixed-rate and hybrid ARM pass throughs), ABS, and CMBS (Agency and non-Agency). ICE BofA US Corporate Index tracks the performance of US dollar denominated, fixed rate, investment grade corporate debt publicly issued and settled in the US domestic market. ICE BofA US Treasury Index tracks the performance of US dollar denominated sovereign debt publicly issued by the US government in its domestic market.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author or speaker, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC.

Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy or, nor liability for, decisions based on such information.

©2024, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. Guggenheim Funds Distributors, LLC is an affiliate of Guggenheim Partners, LLC. For information, call 800.345.7999 or 800.820.0888.

TL-TURNINGPOINTS 61289

Portfolio Management Outlook: Sound Credit Fundamentals and Elevated Yields to Weather Tail Risks to Our Outlook

The Advantages of Investing in Infrastructure and Other Real Assets