Introduction

The U.S. fixed-income market offers some of the best income opportunities in decades. Yet core fixed-income investors benchmarked to the Bloomberg U.S. Aggregate Index (Agg) are forgoing some of the most attractive risk-adjusted returns. The Agg’s composition has lagged the evolution of the fixed-income landscape and now represents less than half of the investable universe. The index is also increasingly concentrated in government-related debt, especially Treasurys. We believe this leaves investors under-diversified and earning lower returns.

Investors tilting heavily toward investment-grade corporate bonds in an effort to overcome this concentration and boost returns may simply be replacing one form of concentration with another—creating asymmetric risk to spread widening. At Guggenheim Investments, we believe a more efficient solution lies in actively managed, diversified portfolios that draw from both benchmark and non-benchmark sectors, including structured credit, private lending, commercial mortgage loans, and other higher quality assets that may offer attractive excess returns, strong structural protections, and stable income.

Report Highlights

- The Agg represents less than half of the investable fixed-income market, and strategies constrained by this benchmark overlook sectors that may offer stable and attractive excess returns with the expertise to manage the complexity.

- At $28.7 trillion, the Agg represents less than half of the total U.S. fixed-income universe, leaving out $30.8 trillion of non-indexed securities.

- While traditional benchmarks like the Agg may not fully capture the breadth of possible fixed-income investment opportunities, a diversified and active approach can help unlock returns by investing across the fixed-income spectrum, including sectors not included in the Agg.

- For established investors like Guggenheim Investments, deep expertise in sourcing structured products and managing credit risk positions our team to potentially generate returns and manage risk across the debt capital structure in a variety of industries.

SECTION 1

The Core Conundrum

With yields at historically attractive levels, fixed income presents one of the most compelling income-generating opportunities in years. Yet the benchmark that many investors rely on—the Agg—has become increasingly misaligned with the opportunity set. Its inclusion criteria have led to overconcentration in Treasurys and limited sector diversification. Credit spreads in many Agg categories are near historically tight levels, providing little cushion to help protect against adverse environments.

Accordingly, we believe investing solely in the indexed universe does not provide the best risk-return tradeoffs for investors. In our view, capturing fixed-income opportunities requires a more flexible approach that goes beyond traditional benchmarks to optimize both yield and risk management.

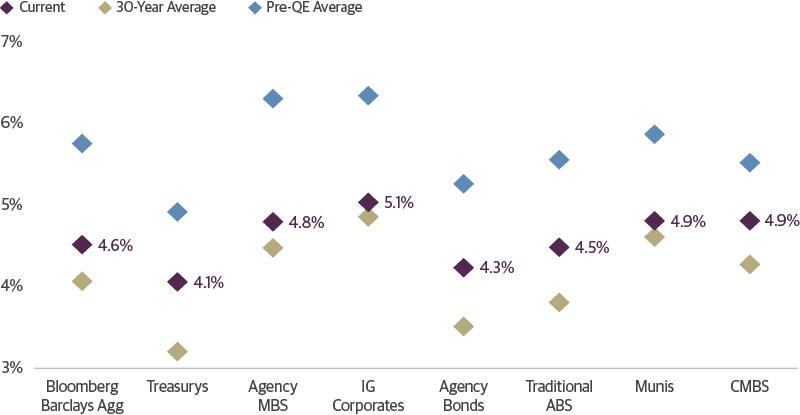

The Income Is Back in Fixed Income

Unique circumstances after the global financial crisis helped keep Treasury yields below 3 percent for almost a decade. Below-mandate inflation, combined with a sluggish economic recovery, led the Federal Reserve (Fed) to maintain a prolonged period of near-zero policy rates and quantitative easing (QE).

Since the pandemic, however, higher quality fixed-income yields have returned to historically attractive levels, creating a compelling opportunity to enhance portfolio income. Yields may fluctuate with the business cycle but seem unlikely to return to the low levels of the previous decade. The recent move higher reflects a return to more normal expectations for long-term growth, supported by solid U.S. fundamentals. From a longer historical perspective, today’s yield levels appear more typical than those of the post-2008 period. Absent a significant shock, we expect them to remain in this higher range.

The Income Is Back in Fixed Income

Benchmark Sector Yields Versus Their Historical Average

Source: Guggenheim Investments, Bloomberg. Data as of 4.30.2025. Index Legend: U.S. Treasurys: Bloomberg U.S. Treasury Index; Agency MBS: Bloomberg U.S. Mortgage Backed Securities Index; IG Corporates: Bloomberg U.S. Corporate Investment Grade Index; Agency Bonds: Bloomberg U.S. Government Bond Index; ABS: ICE BofA AA-BBB US Fixed Rate Asset Backed Index; Municipals: Bloomberg Municipal Bond Index; CMBS (Commercial Mortgage-Backed Securities): Bloomberg Investment Grade CMBS Index. Past performance does not guarantee future results. Investing involves risk, and income is not guaranteed.

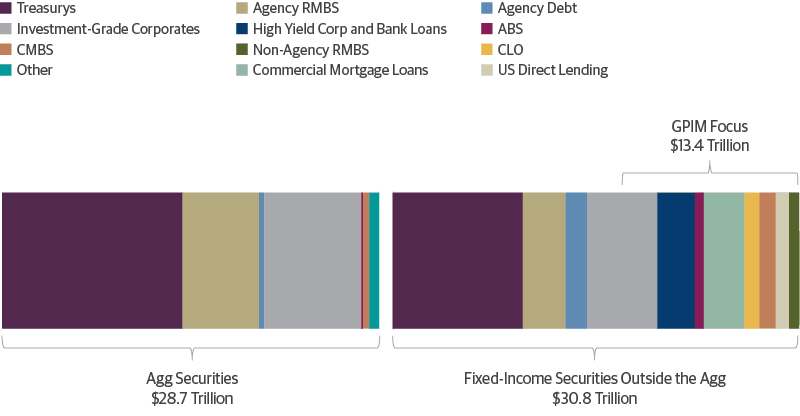

The Agg Fails to Capture the Breadth of Fixed-Income Market Opportunities

Even as overall yields offer higher income, investors relying solely on the Agg will miss the breadth of opportunities available in today’s fixed-income market. The Agg represents less than half of the investable fixed-income market, and strategies constrained by this benchmark overlook sectors that may offer stable and attractive excess returns to investors with the expertise to manage the complexity.

The Agg Fails to Capture the Breadth of Fixed-Income Market Opportunities

The Bloomberg U.S. Aggregate Bond Index Represents Less than Half of the Fixed-Income Universe

Source: Guggenheim Investments, SIFMA, Bloomberg, JP Morgan Research, BofA Global Research, Mortgage Bankers Association. Data as of 12.31.2024.

Originally designed to represent the investment-grade fixed-income universe, the composition and risk profile of the Agg have lagged the evolution of the fixed-income landscape. The index includes only securities that are U.S. dollar-denominated, investment-grade rated by three agencies (Moody’s, S&P, and Fitch), fixed rate, and taxable. The Agg also has minimum issue size requirements that narrow its constituents to larger, less varied bonds.

These features limit inclusion to more liquid issues at the expense of a broad range of fixed-income securities that can offer investors diversification and excess return potential. Key sectors underrepresented or entirely absent from the Agg include asset-backed securities (ABS), collateralized loan obligations (CLOs), residential mortgage-backed securities (RMBS), commercial mortgage-backed securities (CMBS), high yield bonds, commercial real estate (CRE) loans, leveraged loans, and private debt, as well as any floating-rate or tax-exempt securities. Importantly, the Agg excludes privately placed, unregistered securities entirely, limiting its coverage of a large and rapidly growing segment of the fixed-income market.

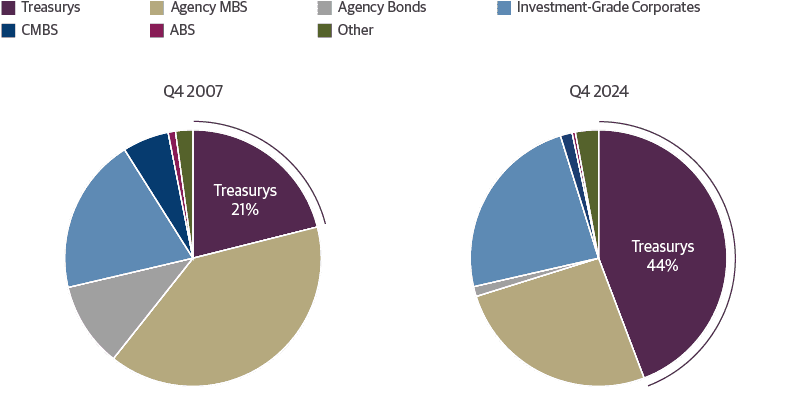

The Agg Is Increasingly Concentrated in Treasury Securities

The sharp rise in federal deficits since 2008 has reshaped the composition of the Agg by dramatically increasing the supply of U.S. Treasurys. Marketable U.S. Treasury securities have grown at an average annual rate of 12 percent since 2009, far outpacing the growth of nonfinancial corporate debt (4 percent) and financial institution debt (1 percent). As a result, the U.S. government has become the dominant borrower in public bond markets. This shift has driven Treasurys’ share of the Agg from just 21 percent in 2007 to 44 percent today—concentrating duration and rate sensitivity in benchmark-constrained portfolios.

Treasurys Used to Be Less than a Quarter of the Agg

Bloomberg U.S. Agg Index, by Sector, Dec 2007

Today, Treasurys Represent 44% of the Agg

Bloomberg U.S. Agg Index, by Sector, Dec 2024

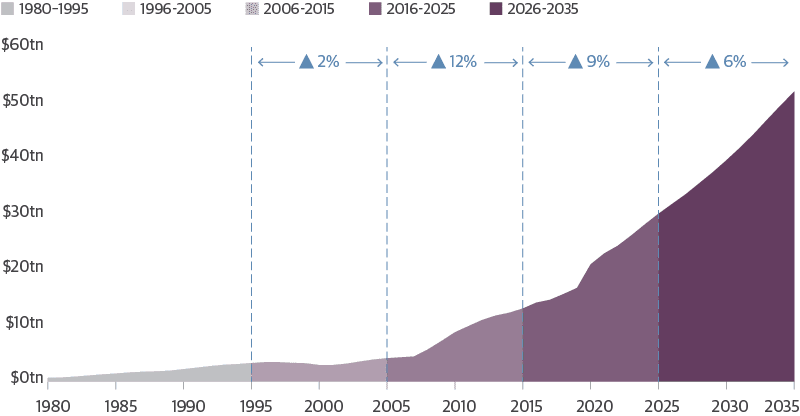

As Treasurys constitute an increasing share of the U.S. bond market, so too will the Agg—and any index-constrained or passive funds—become increasingly overexposed. The Congressional Budget Office (CBO) projects Treasury issuance to rise from $28 trillion today to $52 trillion by 2035, increasing as a share of gross domestic product (GDP) from 98 percent to 120 percent. This upward trajectory reflects rising interest costs as a share of the budget as well as structural challenges to deficit reduction, including the persistence of mandatory spending programs and the political difficulty of enacting durable fiscal reforms even during periods of economic expansion.

Rate volatility may also be structurally higher in the future, presenting a challenge for passive long duration investments. Shifts in global trade, more focus on fiscal policy, and growing investment needs in megatrends like artificial intelligence and infrastructure may lead to more frequent supply shocks and episodic inflation. These dynamics increase the likelihood of more variable monetary policy and higher implied volatility compared to the period from 2010–2019, which was characterized by expectations for low and stable policy rates. As such, the environment for interest rates appears to be entering a phase that favors active management.

Treasurys Outstanding Surged Post-2007 and Will Continue to Rise

Treasury Securities Outstanding in $Trillions

Better Opportunities Beyond the Benchmark

Fixed income plays an important role in the portfolios of long-term investors by buffering downside risk through diversification and providing steady income to match assets and liabilities, but the Agg alone may not provide the yield or diversification longer-term investors are seeking. Pension plan managers and other investors seeking to match long-term liabilities face challenges meeting high return requirements. The National Association of State Retirement Administrators reports that the median investment return assumption for national public pension plans is 6.9 percent, while life insurers typically target 5–6 percent for annuity products.

These targets are typically met with blended equity/bond portfolios, but they highlight the need for investors to achieve strong returns and broad diversification from fixed income. With its limited coverage of the fixed-income universe and concentration in government securities, the Agg is not meeting these requirements.

SECTION 2

Stretching for Yield to Overcome Agg Concentration

In seeking to overcome the benchmark’s inability to meet return or diversification needs, investors are increasingly overweighting higher yielding sectors within the index—particularly investment-grade corporates—and many are doing so through passive strategies. This introduces new vulnerabilities: increased exposure to lower rated credit, limited compensation for risk, and reduced flexibility to navigate volatility. Understanding these tradeoffs is critical to building more resilient fixed-income portfolios.

Investors May Be Taking on Undue Credit Risk Within the Agg

Core fixed-income investors who have some flexibility to adjust weightings may tilt heavily toward the investment-grade corporate bond market. Passive exposure to corporates in the Agg carries a structural bias toward lower quality credit, introducing greater downgrade risk in an economic downturn. BBB-rated bonds have grown from less than 30 percent of the investment-grade universe in the late 1990s to nearly half of the Bloomberg U.S. Corporate Bond Index today.

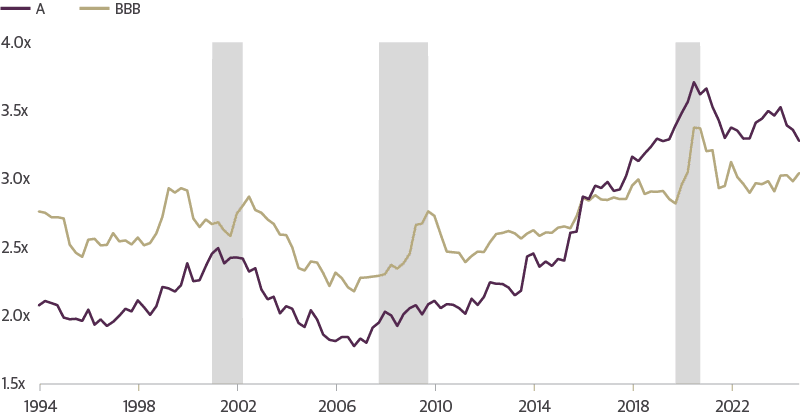

While current yields are attractive, indexed credit spreads are tight. As a result, they make up a smaller share of all-in yields—averaging less than 20 percent since 2023 versus a historical average of almost 30 percent. Spreads across all investment-grade corporate ratings have hovered near the low end of their historical range, leaving little buffer if market expectations around growth shift.

Leverage ratios are also currently higher for A-rated and BBB-rated issuers relative to their history, leaving these issuers more vulnerable to downgrades than would typically be the case.

An Increasingly BBB Rated Investment-Grade Market Raises Spillover Risks

BBB as % of Investment-Grade Corporate Index

Source: Guggenheim Investments, Bloomberg. Data as of 1.31.2025. Gray areas represent recession.

Credit Spreads Are Approaching Historical Tights

A-Rated and BBB-Rated Corporate Bond Option-Adjusted Spreads

Source: Guggenheim Investments, Bloomberg. Data as of 4.30.2025. Gray areas represent recession.

Higher Leverage Could Make the Investment-Grade Sector More Cyclical

Median Gross Leverage, A through BBB-Rated Nonfinancial Corporates

Source: Guggenheim Investments, Bloomberg. Data as of 12.31.2024. Gray areas represent recession.

Passive Fixed-Income Investing Remains Dominant

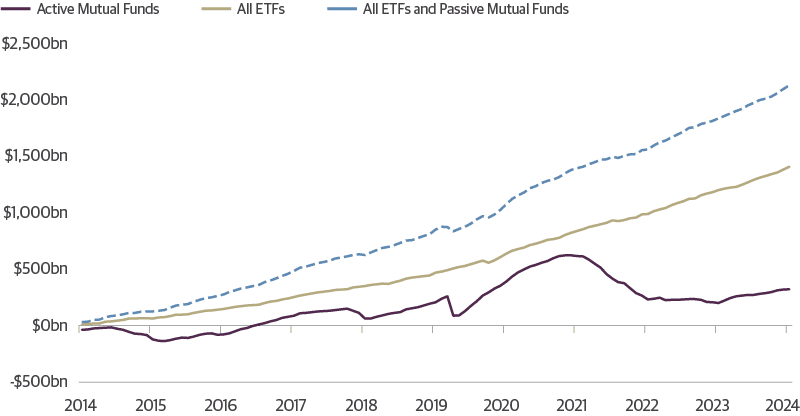

Despite tight spreads and a more turbulent fixed-income environment, investors have increasingly allocated to passive fixed-income strategies in recent years. Roughly $1.2 trillion in institutional assets are now managed in index-tracking vehicles, alongside an estimated $2.1 trillion in passively managed taxable bond mutual funds and ETFs.

By design, passive strategies lack the flexibility to actively manage risks or capitalize on price dislocations when market conditions shift. In addition, index-tracking vehicles lock investors into the Agg universe of investments, increasing the commoditization of this fixed-income universe.

The large and growing reliance on passive fixed income also warrants caution. While passive vehicles are often favored for perceived liquidity, periods of market stress tend to trigger concentrated outflows. This dynamic can exacerbate volatility, as asset managers are forced to sell into weakening markets to meet redemptions—introducing a structural layer of risk that investors may underappreciate

Passive Strategies Are Still Desired by Fixed-Income Investors

Cumulative Net Flows into Taxable Fixed-Income Strategies

Source: Guggenheim Investments, Morningstar. Data as of 12.31.2024.

SECTION 3

Guggenheim’s Investment Blueprint

At Guggenheim Investments, we believe in a disciplined strategy that combines active management within the benchmark and selective allocations beyond it without sacrificing quality. Structured credit, direct lending, commercial real estate (CRE) loans, and military housing has offered compelling opportunities to enhance diversification, maintain liquidity, and generate attractive yields. But investors must approach these out-of-benchmark allocations with prudence, trusting a manager with the deep expertise, relationships, and resources to navigate their unique challenges.

Active Management Is Crucial in a Higher Volatility Regime

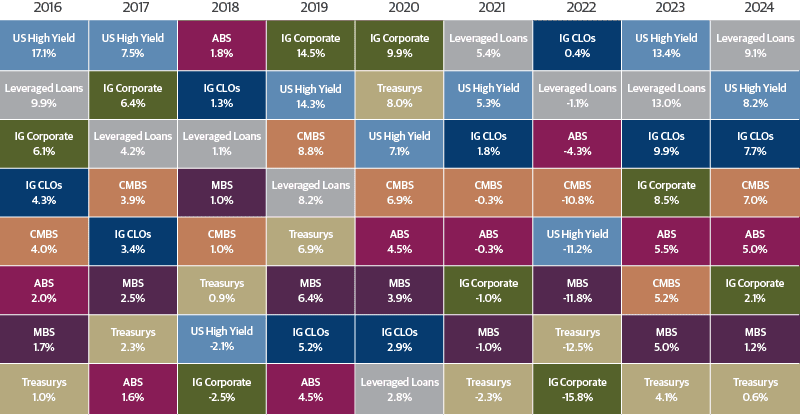

Fixed-income returns are rarely consistent from year to year, favoring managers that can capitalize on emerging opportunities. The performance leadership among sectors shifts frequently, with leveraged loans, high yield, investment-grade corporate bonds, and structured credit each taking turns at the top. This rotation creates opportunity for active managers to add value by adjusting allocations across sectors. Capturing that value requires a disciplined and time-tested investment process grounded in research. Of course, there will be periods when the Agg will outperform an active fixed-income manager but, over a cycle, capable active managers should be able to find opportunity and limit risk in in a manner that achieves better results for their clients.

Asset Allocation Matters

Sector Index Returns

A World Beyond the Benchmark: Specialized Credit Markets

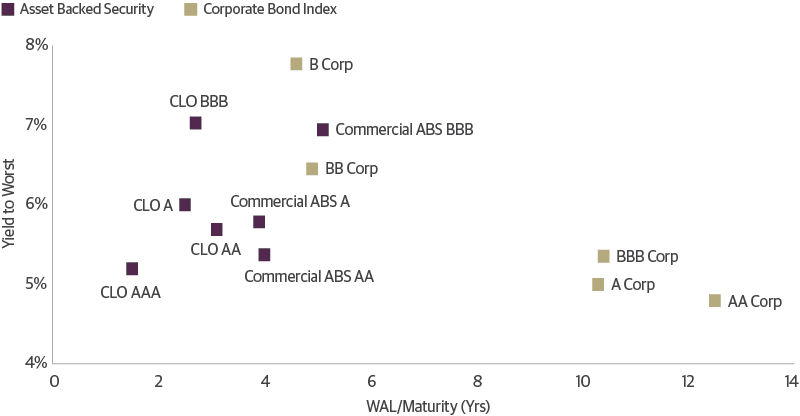

We believe some of the most attractive opportunities in fixed income lie beyond the benchmark in specialized credit markets that typically offer better structural protections, stronger cash flow profiles, and greater complexity premiums. In an environment in which risk premiums remain tight, simply moving up in credit rating is not enough. Investors must redefine “up in quality” by focusing on sectors that typically offer greater resilience across cycles. But these sectors are varied and complex, requiring managers with deep expertise and relationships to take advantage of opportunities.

Structured credit is one area in which we have consistently found value over time. The sector offers distinct advantages, including broader diversification across ratings, structures, and underlying assets. It has a demonstrated history of credit resilience, outperforming similarly rated corporate debt in terms of credit rating migration and default trends. The asset class also typically offers higher yields and spreads relative to comparably rated corporates due to their complexity.

We apply the same selective, research-driven approach across other specialized markets. Direct lending, a subset of what investors broadly refer to as private debt, provides an opportunity to originate loans with enhanced structural protections and relative credit strength. In a market crowded with new entrants, Guggenheim Investments brings over 20 years of direct lending experience, having invested more than $25 billion across 450 middle-market loans through a disciplined and scalable underwriting process.

Niche sectors with limited investor participation can also offer compelling opportunities. Military housing, financed through long-term public-private partnerships, benefits from indirect government support, strong occupancy demand, and stable contractual cash flows tied to military housing allowances. These assets have no recorded history of default. In CRE, opportunities continue to emerge even as recent challenges in the office sector underscore the importance of active credit selection. The sector offers diversity in ratings and customized structural features and has historically exhibited low correlation to other fixed-income sectors, helping to enhance portfolio diversification.

Discovering Yield in Structured Credit

Sector Yields vs. Sector Maturity

Guggenheim Is Well-Positioned to Solve the Core Conundrum

The fixed-income landscape in 2025 presents some of the most attractive opportunities in decades, but also significant challenges. While traditional benchmarks like the Agg may not fully capture the breadth of possible fixed-income investment opportunities, a diversified and active approach can help unlock returns by investing across the fixed-income spectrum, including sectors not included in the Agg. With the chasm between investors’ income targets and benchmark yields likely to persist, traditional views of core fixed-income management need to evolve. In our view, investors must be willing to look beyond the benchmark to explore sectors in which value remains underexploited. This approach demands significantly more credit expertise and ongoing diligence, but we believe it offers the prospect of better risk-adjusted returns over time. For established investors like Guggenheim Investments, deep expertise in sourcing structured products and managing credit risk positions our team to potentially generate returns and manage risk across the debt capital structure in a variety of industries.

Important Notices and Disclosures

The Bloomberg U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, US dollar-denominated, fixed-rate taxable bond market.

The index includes Treasurys, government-related and corporate securities, MBS (Agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS (Agency and non-Agency).

The Bloomberg U.S. Aggregate ABS Index is component of the Bloomberg U.S. Aggregate Index, the Bloomberg U.S. Aggregate ABS Index includes pass-through, bullet and controlled amortization structures. The Index includes only the senior class of each ABS issue and the ERISA-eligible B and C tranche.

The Bloomberg U.S. CMBS Investment-Grade Index measures the market of U.S. Agency and U.S. non-Agency conduit and fusion CMBS deals with a minimum current deal size

of $300m.

The Bloomberg U.S. Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD denominated securities publicly issued by U.S. and non-U.S. industrial, utility, and financial issuers.

The Bloomberg U.S. MBS Index consists of the MBS assets within the Bloomberg Aggregate Index.

The Bloomberg U.S. Municipal Bond Index is a broad-based benchmark that measures the investment grade, USD-denominated, fixed tax-exempt bond market. The index includes state and local general obligation, revenue, insured, and pre-refunded bonds.

The Bloomberg U.S. Treasury Index measures U.S. dollar-denominated, fixed-rate, nominal debt issued by the U.S. Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index. STRIPS are excluded from the index because their inclusion would result in double-counting.

The Bloomberg U.S. Corporate High-Yield Bond Index measures the USD-denominated, high yield, fixed-rate corporate bond market. Securities are classified as high yield if the middle rating of Moody’s, Fitch and S&P is Ba1/BB+/BB+ or below.

The S&P UBS Leveraged Loan Index is designed to mirror the investable universe of the USD-denominated leveraged loan market.

The ICE BofA U.S. Fixed & Floating Rate Asset Backed Securities Index tracks the performance of USD-denominated investment-grade asset backed securities publicly issued in the US domestic market.

The ICE BofA AA-BBB U.S. Fixed Rate Asset Backed Index is the AA-rated to BBB-rated subset of the ICE BofA U.S. Fixed Rate Asset Backed Securities Index, which tracks the performance of USD-denominated investment-grade fixed rate asset backed securities publicly issued in the U.S. domestic market.

The Palmer Square CLO Senior Debt Index is also a rules-based observable pricing and total return index for CLO debt for sale in the United States, rated at the time of issuance as AAA or AA or equivalent rating. Such debt is often referred to as the senior tranches of a CLO.

The Palmer Square CLO Debt Index is a rules-based observable pricing and total return index for collateralized loan obligation debt for sale in the United States, original rated A, BBB, or BB or equivalent rating.

Past performance does not guarantee future results.

Investing involves risk, including the possible loss of principal. In general, the value of a fixed-income security falls when interest rates rise and rises when interest rates fall. Longer term bonds are more sensitive to interest rate changes and subject to greater volatility than those with shorter maturities. During periods of declining rates, the interest rates on floating rate securities generally reset downward and their value is unlikely to rise to the same extent as comparable fixed rate securities. High yield and unrated debt securities are at a greater risk of default than investment grade bonds and may be less liquid, which may increase volatility. Investors in asset-backed securities, including mortgage-backed securities and collateralized loan obligations (“CLOs”), generally receive payments that are part interest and part return of principal. These payments may vary based on the rate loans are repaid. Some asset-backed securities may have structures that make their reaction to interest rates and other factors difficult to predict, making their prices volatile and they are subject to liquidity and valuation risk. CLOs bear similar risks to investing in loans directly, such as credit, interest rate, counterparty, prepayment, liquidity, and valuation risks. Loans are often below investment grade, may be unrated, and typically offer a fixed or floating interest rate. Private debt investments are generally considered illiquid and not quoted on any exchange; thus they are difficult to value. The process of valuing investments for which reliable market quotations are not available is based on inherent uncertainties and may not be accurate. Further, the level of discretion used by an investment manager to value private debt securities could lead to conflicts of interest. There is no guarantee that an active manager’s views will produce the desired results or expected returns, which may lead to underperformance. Actively managed investments generally charge higher fees than passive strategies, which could affect performance. In addition, active and frequent trading that can accompany active management, also called “high turnover,” may lead to higher brokerage costs and have a negative impact on performance. Further, active and frequent trading may lead to adverse tax consequences.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

© 2025, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC. Guggenheim Funds Distributors, LLC is an affiliate of Guggenheim Partners, LLC. For information, call 800.345.7999 or 800.820.0888.

65189

The Advantages of Investing in Infrastructure and Other Real Assets

Portfolio Management Outlook: Staying Focused Amid Geopolitical Uncertainty