A version of this article appeared in the Insurance Asset Management North America 2022 report.

Fixed-income portfolio managers face a challenge we call the Core Conundrum: In this period of historic low rates, where to find yield? Our approach to solving the Core Conundrum is in sourcing, researching, and allocating to sectors which typically are not included in the broad industry benchmark index, the Bloomberg U.S. Aggregate Bond Index (the Agg). In addition to this already difficult challenge, insurance companies have additional conundrums layered on top, including unique asset-liability challenges, increasingly restrictive accounting requirements, dependency on external ratings, and, most importantly, onerous regulatory requirements. These multi-faceted problems facing the insurance industry are making it harder for life insurers to operate in the competitive financial marketplace.

While the recent backup in rates provides some rays of hope, purchase yields are still trending below portfolio rates. Exacerbating the issue of low yields, many insurance products contain minimum rate guarantees. Those minimums on legacy insurance products can be upward of 4 percent. With such rich guarantees, policyholders are holding on to policies longer, which is extending duration. This in turn can lead to negative margins on a large swath of policies over a long period of time. All the while, regulations require insurance companies to hold sufficient capital to support the business. This has led to a highly inefficient use of capital, causing many insurance companies over the past decade to sell off legacy businesses to allow for reallocation of capital to higher-returning businesses. Simply put, the impact of pricing mistakes or asset liability mismatches from a decade or two ago can lead to very weak returns, forcing many insurance companies into strategic reviews of their in-force business.

The Core Conundrum

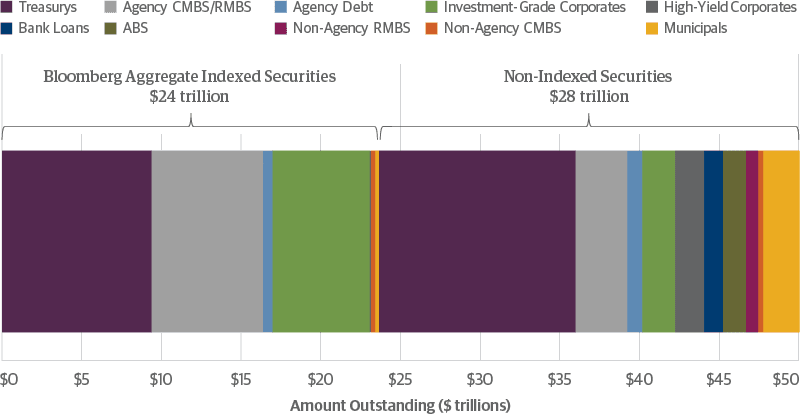

The common denominator for all fixed-income investors is the dearth of yield, which is in large part a consequence of extraordinary monetary easing in response to two global crises over the past 15 years. Since its creation in 1986, the Agg has been the most widely used proxy for the U.S. bond market. However, the broad fixed-income universe has evolved over the past 36 years with the growth of sectors such as asset-backed securities (ABS), non-Agency residential mortgage-backed securities (RMBS), high-yield corporate bonds, leveraged loans, and tax-exempt municipal bonds.

While the fixed-income universe has become more diversified in structure and quality, the composition of the Agg has not kept pace with these changes. Treasurys today comprise 49 percent of the Agg, which, when combined with Agency securities, brings the weighting of U.S. government-related debt to just over 76 percent of the Agg. Thus, investors reluctant to stray far from the Agg’s composition are disadvantaged by sector concentration in low yielding securities.

The sheer glut of Treasurys and their dominant representation in the Agg is unlikely to reverse anytime soon due to the ongoing need to fund government deficits—present and future.

Fixed-Income Markets Are Underrepresented by the Agg

The Bloomberg U.S. Aggregate Bond Index Represents Less than Half of the Fixed-Income Universe

Traditional yield-enhancement techniques, such as increasing duration and lowering credit quality, may boost total returns in the short term, but easy financial conditions may be masking the risks associated with potentially damaging long-term effects of reflating the economy through debt accumulation. We believe there is a more sustainable strategy that relies on the ability to uncover value in predominantly investment-grade securities outside of the traditional benchmark-driven framework.

The Insurance Company Hunt for Yield Amid Tightening Regulations

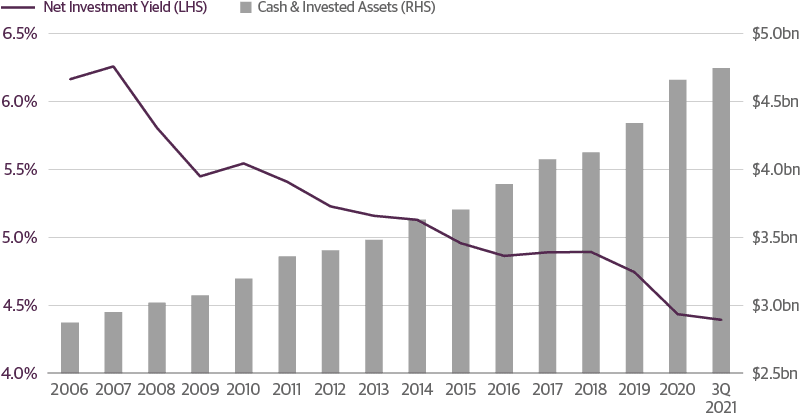

Over the last decade, declining insurance portfolio yields have led companies to solve the Core Conundrum by seeking out higher-yielding assets in which they had not historically participated, such as structured credit and private credit. Others looked to introduce equity-like returns into their bond portfolio by using hybrid investment vehicles, some of which mirror to a degree the policy structures that insurers sell to policyholders. One such policy structure is the fixed indexed annuity, which has been added to the shelf of practically every life insurer in recent years and provides upside potential to policyholders based on the performance of an underlying index. It also includes protection through a minimum guarantee.

Insurance Portfolio Yields Have Continued to Decline

At the same time insurers are searching for yield, over the past several years the National Association of Insurance Commissioners (NAIC), as advised by the Securities Valuation Office (SVO), has become increasingly suspect of certain assets classes in insurance company portfolios and predisposed to increase capital requirements on those investments. Historically, under the prescribed rules, insurers relied on the fact that once a bond was rated by a nationally recognized statistical ratings organization (NRSRO), the bond was deemed exempt from filing. This filing exemption allowed a direct conversion from one or multiple ratings to an NAIC designation, leading to the determination of required capital. This framework provided insurers with a clear roadmap of the capital required to back the specific mix of assets in a portfolio. Recently, this bedrock premise of rating and capital requirement has been under attack on several fronts. As of year-end 2021, Principal Protected Securities and Combo Notes no longer have filing exemptions, which means insurers can no longer forecast capital requirements on a NRSRO rating alone, but must now file the security with the SVO and wait for their conclusion in hindsight. In other words, the NRSRO rating is no longer the determining factor for the required capital on the investment, limiting the insurers ability to know with certainty the cost of allocating capital to an investment. In many situations, the SVO’s designation on the security is substantially lower, which may make the investment uneconomic, often months after the fact.

The NAIC is also looking to limit the filing exemption process in other ways. For private letter ratings, insurers now are required to file a credit package with the SVO for review before being able to utilize the NRSRO rating. In addition, the NAIC is looking at the potential of requiring two ratings on private securities, essentially limiting or eliminating NRSROs that can be used in the designation process.

The NAIC is additionally engaging in a fundamental re-examination of what qualifies under the accounting guidance in SSAP 43R and SSAP 26, and in turn what gets reported in the Schedule D, Schedule BA, and potentially a new schedule within the insurer’s Statutory Annual Statements. The disposition of this matter currently remains in flux but there is little doubt that it will proceed in some fashion, with potentially far-reaching and long-lasting impact to insurers’ capital and accounting requirements, and their ability to write new business.

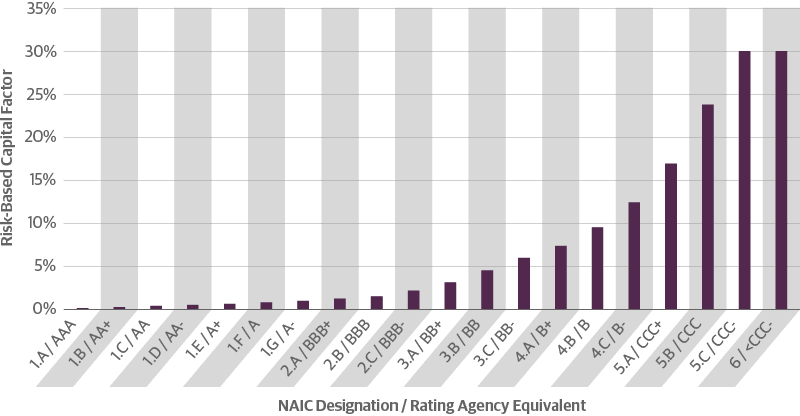

This increased level of oversight, and the assumption that non-vanilla investment products are riskier for insurance companies, is having a detrimental effect on insurers. Besides the lack of clarity and consistency, and increased time needed to transact, this is having a direct economic impact on the business. Every asset on an insurance company’s balance sheet has an associated designation and capital charge. While asset risk is only one of several risks for which insurers need to maintain capital, for life insurers—and particularly for annuity focused writers—it is the largest. As demonstrated in the following chart, the resulting capital factor seeking to capture the underlying credit risk is parabolic.

Capital Requirement Rises Exponentially Per NAIC Designation

Most insurers target a capital ratio of at least 350 percent, which means that increased requirements for certain assets can lead to needing to hold disproportionate levels of capital for the asset, thereby making it an uneconomic fit for the portfolio. For example, a downgrade of a security from a 1.G designation to a 4.C designation would lead to an approximate 12x increase in the capital required. This is especially troublesome for existing securities in portfolios that were acquired under prior rules that now have to be re-examined and potentially jettisoned into an illiquid market.

At a time when it is vital for insurers to find differentiated investments, these shifting requirements are essentially forcing them to become index investors. It steers insurers into lower-yielding core asset classes, further pressuring investment yields.. Indirectly, insurance company policyholders (and shareholders) are potentially compromised by the narrowing investment opportunities to which insurers have access, which may lead to lower crediting rates and higher insurance costs.

Solving the Insurance Company’s Investment Conundrums

All of these factors are forcing insurance companies to once again confront the core conundrum facing all fixed-income investors: How to meet their total return objectives without taking on undue risk?

First, difficult times calls for a disciplined approach. Insurers must carefully price new products with achievable targets and margins. There must be clear and consistent communication across the various business units from design to sale. Actuarial and product design teams must partner with investment and sales team to target achievable goals. After all, introducing teaser rates on new products end up being just that, and insurers typically live to regret having accumulated an unattractive set of liabilities.

Second, insurers need to be much more active in voicing their concerns about regulation and not wait on a few voices to drive the narratives. Insurers should be more proactive with their individual state regulators to show the other side of the impact of overregulation and involvement by the SVO in security ratings already well covered by nationally recognized firms that are regulated by the SEC. Well-designed and debated regulation is always necessary and warranted, but the broad sweeping regulation engulfing the industry now is throwing out the baby with the bathwater. Regulation should be more principles-based, with oversight directed at perceived abusers as opposed to imposing onerous and impractical constraints on the entire industry at a time when it is already facing significant challenges meeting yield and duration targets.

Third, insurers must take advantage of the unique nature of their liabilities. The illiquidity of their liabilities allows for insurers to similarly take additional illiquidity risk on the asset side of the balance sheet, a strategy that has been successfully deployed with other institutional investors with long-lived liabilities, including endowments and foundations.

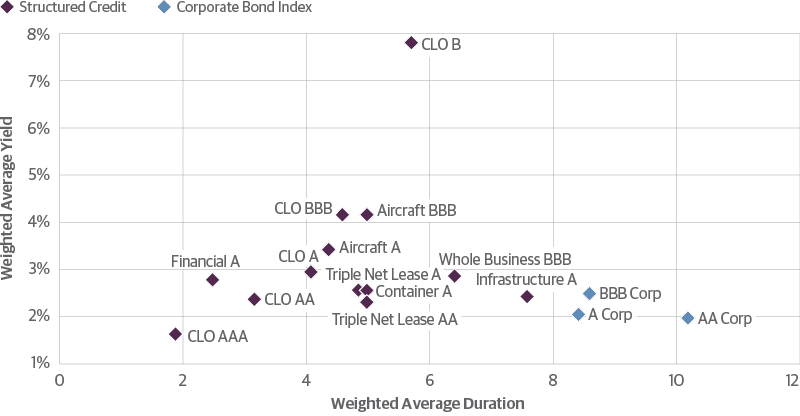

Our history of managing assets for insurance companies has demonstrated that managing duration within tolerable constraints, maintaining an investment-grade portfolio, and generating attractive yields do not have to be competing investment objectives. Investment-grade assets exist outside the traditional benchmark, and can offer attractive yields that are comparable to, or higher than, similarly rated corporate bonds, such as structured credit.

Discovering Yield in Structured Credit

We believe that investment strategies that will solve the Core Conundrum have the best potential to harvest superior risk-adjusted returns for insurance clients in the current fixed-income market environment. With the chasm between insurance companies’ income targets and benchmark yields likely to persist, traditional views of core fixed-income management need to evolve. In our view, investors must be willing to look beyond the benchmark to explore sectors in which value remains underexploited. Changes in regulation will continue to pressure results in today’s market. Insurance companies understand this and have begun moving beyond the benchmark to seek to generate superior risk-adjusted returns. The challenge now is whether the changes coming in statutory classification, accounting, ratings, and capital requirements will hamper these efforts and make an already difficult business even more difficult.

Important Notices and Disclosures

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author or speaker, but not necessarily those of Guggenheim Partners, LLC or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information. No part of this material may be reproduced or referred to in any form, without express written permission of Guggenheim Partners, LLC.

Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy or, nor liability for, decisions based on such information.

©2022, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.

51544

The Advantages of Investing in Infrastructure and Other Real Assets

Portfolio Management Outlook: Staying Focused Amid Geopolitical Uncertainty