Summary

The demand for infrastructure investment is surging, driven by decades of underinvestment, evolving demographics, and the transformative secular forces of digitalization, deglobalization, and decarbonization. This rising need coincides with a pullback from traditional financing sources, creating a multi-trillion-dollar funding gap. Private capital is increasingly stepping in to address this shortfall, presenting a compelling opportunity for investors seeking stable, long-term returns.

This report explores the dynamic landscape of infrastructure investing, highlighting the diverse opportunities across sectors and the risk-return spectrum. From essential services like transportation, digital infrastructure, and the energy complex powering our modern world, we examine the potential benefits of investing in infrastructure assets, including steady cash flow, inflation protection, portfolio diversification, and resiliency through economic cycles. We also delve into the strategic advantages of focusing on the middle market, where a less competitive environment can yield attractive valuations and stronger covenant protections.

Report Highlights

- Infrastructure investment needs are surging due to decades of underinvestment, demographic shifts, and the secular megatrends of digitalization, deglobalization, and decarbonization. Meanwhile, traditional financing sources have scaled back, leaving a multi-trillion-dollar funding gap that private capital is increasingly filling.

- Because many infrastructure assets provide essential services, demand for which often does not vary with the economy or interest rates, they can offer a compelling combination of steady cash flow, portfolio diversification, and a hedge against both inflation and recession. They range from stable, low risk core assets to high risk, high return opportunistic investments, catering to different investor objectives.

- We believe there is better relative value in the middle market, ranging from $50 million to $500 million, which offers a more plentiful, diverse investment landscape with fewer bidders than in the large-cap market.

- The size and complexity of the infrastructure investment landscape present a challenge. Successful infrastructure investing requires entrenched long-term relationships with borrowers, sponsors and banks, sector expertise, as well as dedicated underwriting and origination teams with experience across private and public debt and equity.

- Guggenheim’s approach to investing in hard assets—or tangible, physical investments—leverages our scale and deep underwriting expertise across dedicated infrastructure, real estate, and structured product franchises. Extensive industry relationships provide differentiated investment opportunities, providing us with increased opportunities to unlock value with a focus on risk-adjusted returns.

Infrastructure Investing: Driving and Driven by Dynamic Global Change

The need for investment in infrastructure is set to surge in the coming years, driven by decades of underinvestment, socio-demographic shifts, and the massive secular forces of digitalization, deglobalization, decarbonization. These multi-decade trends will drive demand spanning a diverse range of real assets necessary to move people, goods, energy and resources, and digital information.

Lifestyles have evolved, and infrastructure is evolving with it. Today, we work from smart homes, drive electric vehicles, and make online purchases delivered to our door. Many have moved away from the cities and denser suburbs, in favor of less populated areas. Our lives today require more complex digital, logistical, and transportation infrastructure, fueled increasingly by renewable energy. Meanwhile, deglobalization is reordering global supply chains, further boosting the need for domestic infrastructure. These trends will, in our view, fuel investment opportunities across the risk-return spectrum.

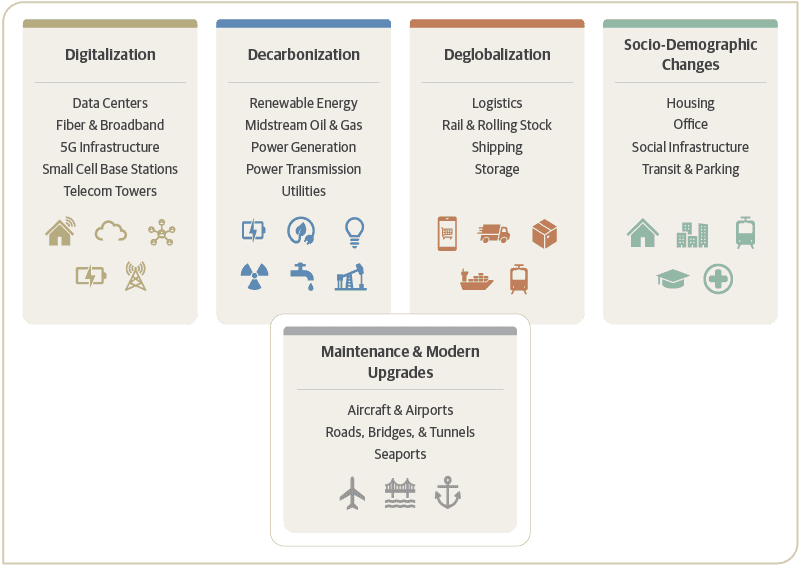

Infrastructure Powers Goods, People, Energy, and Information

Guggenheim Investments’ Focus Areas

Source: Guggenheim Investments.

Digitalization requires the storage and movement of digital information, driving demand for data centers, fiber networks, and 5G infrastructure. The explosive growth of generative AI, cloud computing, Internet of Things (IoT), and bandwidth-intensive applications makes digital infrastructure essential for ensuring fast, secure, and reliable data transmission to power the global economy. Infrastructure investments that will help advance global digitalization include:

- Data centers

- Fiber & broadband networks

- 5G Infrastructure

- Small cell, low power base stations

- Telecom towers

Decarbonization. The clean energy transition is powering ahead despite Congress’ passage of the “One Big Beautiful Bill” in July 2025, which rolled back many of the tax credits and funding mechanisms established under the Inflation Reduction Act (IRA). Incentives for wind, solar, and electric vehicles are being cut, but support for nuclear, geothermal, carbon capture, and battery storage remains largely intact.

Even so, solar and wind remain competitive. Costs keep falling. Market demand is strong. Battery storage is rapidly becoming more cost-effective, easing integration of renewables.

The bigger picture? The need for new energy infrastructure is immense, and the rise of AI is making it even more pressing. Power generation, transmission lines, storage solutions—every link in the chain requires investment. Federal cutbacks may slow some areas but create openings elsewhere. Public-private partnerships in nuclear and geothermal look promising, while states are increasingly taking the lead: New Jersey and Illinois are driving adoption with incentives and equity-focused legislation; Texas through deregulated markets that speed deployment even without federal backing. Financing the future of energy also means investing in grid innovations, scaling carbon capture, and building the skilled workforce needed to build and maintain the next-generation energy system.

Core Clean Energy Transition Investments include:

- Energy (nuclear, geothermal, solar, wind, hydro, etc.)

- Grid Modernization (transmission, distribution, smart grids)

- Energy Storage (batteries, pumped hydro, etc.)

- Electric Vehicle Infrastructure (charging stations, grid updates

The move to accelerate decarbonization will also take the form of a number of peripheral infrastructure investments, including:

- Specialty Equipment Leasing for power projects

- Labor Agencies focused on energy transition sectors

- Peaking Generation Facilities for grid stabilization

- Low Carbon Offshore Oil/Gas Infrastructure

Deglobalization. Reshoring and nearshoring are gaining momentum as geopolitical tensions and protectionist policies slow global trade. These shifts are reshaping the flow of goods and fueling demand for U.S. investment in logistics, transportation, energy, and commercial real estate. According to the Counselors of Real Estate, the nation’s core logistics region—often referred to as the “Golden Triangle,” stretching from the Great Lakes down to Texas and across to the Mid-Atlantic—accounts for more than half of U.S. GDP and is positioned for even greater development demand1. This demand will take the form of numerous new plants and other hard assets that will call for modern infrastructure and commercial real estate to support evolving supply chains.

- Logistics

- Transportation

- Energy

- Commercial real estate

- Aviation

Socio-Demographic Shifts. Migration from urban to suburban and rural areas, the aging of the population, and the trend toward more single-person households are reshaping where and how people live, work, and consume goods and services, creating infrastructure needs in a broader geographic region across residential, commercial, and logistics sectors. These trends are bolstering demand for modern assets, including those that are well-connected and equipped with the latest technologies, driving further investment opportunities in these non-urban areas.

- Residential real estate

- Commercial real estate

- Supply chain logistics

Private Capital Steps In to Fill Growing Funding Gap

The scale of U.S. infrastructure investment required far exceeds what current capital flows can meet, leaving an onerous funding gap. The American Society of Civil Engineers estimates that the investment gap needed to address aging infrastructure total $3.7 trillion this from 2024 through 2-332, across all of its 19 infrastructures–and while federal, state, and local governments typically own roads, water systems, aviation networks, and other societal assets, over 80 percent of non-defense infrastructure is privately owned3

Historically, private sector infrastructure was financed by banks and public debt, along with private and public equity. However, banking regulations implemented after the great financial crisis made infrastructure lending less profitable, prompting banks to scale back.

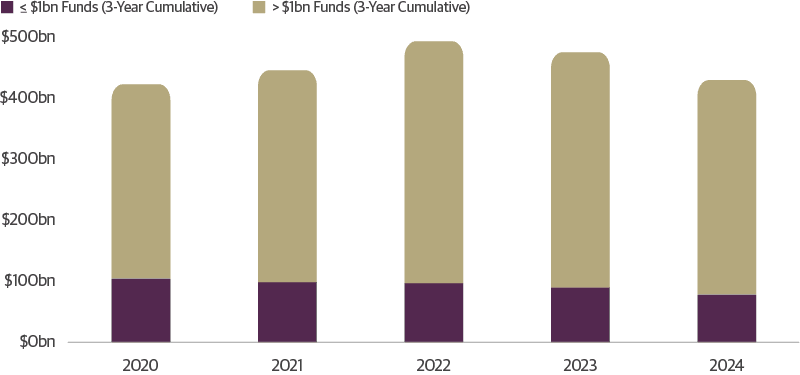

Private capital, attracted by compelling returns, has been increasingly stepping in to fill the gap, now providing almost half of all infrastructure debt and equity financing.4 In the U.S., more than $2.5 trillion poured into the asset class from 2018 through 2022, leading to far larger infrastructure investment funds. The average fund is now more than $4 billion, with more than half exceeding $11 billion.5 In 2023, funds with more than $1 billion in assets under management (AUM) accounted for 83 percent of all real asset strategy fundraising.

Half of the capital raised by these large funds from 2018 through 2022 has yet to be invested. Sitting on this mountain of dry powder, big funds are increasingly vying for the same large infrastructure projects, which may have the effect of driving up valuations. In contrast, smaller funds (under $1 billion in AUM) have just 30 percent of their 2018-2022 vintages uninvested. These smaller funds typically target projects valued from $50 to $500 million, known as the “middle market,” which potentially offers a larger, more diverse landscape, broader exit opportunities, and fewer bidders. Mid-size companies are often overlooked by bigger funds, reducing competition in this market segment.

1. Counselors of Real Estate (CRE), “2023–2024 Top Ten Issues Affecting Real Estate. 2. ASCE estimates that the gap will be $3.7 trillion between 2024 and 2033 if Congress continues recent funding levels. However, that gap would increase substantially if Congress reverts to funding levels in place prior to increases from legislation passed during the Biden administration through the Infrastructure Investment and Jobs Act (IIJA) and Inflation Reduction Act (IRA) 3. CATO Institute, American Society of Civil Engineers. 4. As of 3.31.2025. 5. Pitchbook.

Smaller Funds’ Limited Dry Powder Favors Middle Market Deals

Hard Assets Fundraising by Fund Size – Last Five Years ($Billions)

Source: Pitchbook; as of 3.31.2025. There is no guarantee that any historical trends will continue.

Why Invest in Infrastructure?

Infrastructure investments, typically considered alongside private credit, private equity, and real estate, offer a combination of benefits that distinguish them as a compelling asset class.

Many infrastructure assets provide essential services, the demand for which tends to remain stable regardless of economic conditions or interest rate fluctuations. This characteristic allows infrastructure to potentially offer steady cash flow, resiliency through market cycles, and valuable portfolio diversification. Additionally, infrastructure often provides services through long-term private or government contracts with price escalators tied to inflation, further strengthening its role as an inflation hedge. Private infrastructure also exhibits a significantly lower correlation to public equity than bonds, providing a more effective recession hedge. This resilience is largely due to the asset class’s demand inelasticity and inflation hedging characteristics.

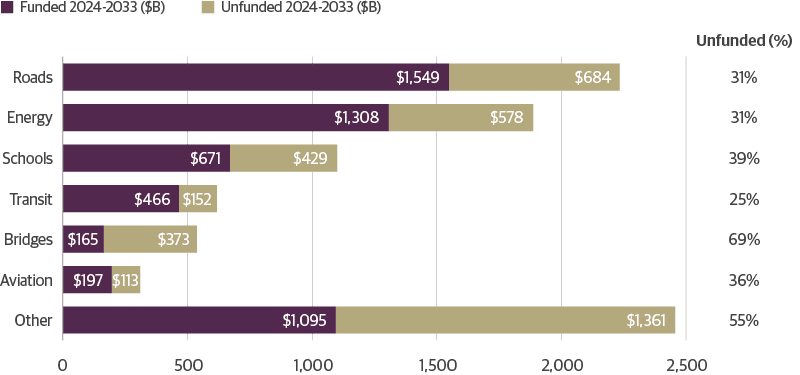

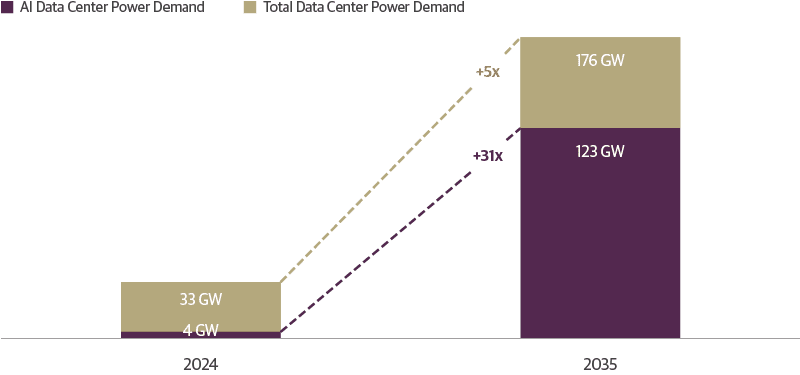

The large projected infrastructure gap and soaring demand for new data centers will, in our view, create significant investment opportunities over the next decade.

America’s $3.8T Infrastructure Gap Creates Significant Investment Opportunities

Source: American Society of Civil Engineers (March 2025). 2025 Report Card for America’s Infrastructure. Funded totals are based on data as of May 2024.

U.S. Power Demand from AI Data Centers Is Expected to Substantially Increase

Source: Deloitte Center for Energy & Industrials analysis of data from DC Byte, Wood Mackenzie, S&P Global, Lawrence Berkeley National Laboratory, Center for Strategic and International Studies, and Wells Fargo. These projections are highly uncertain and dependent on numerous assumptions about AI adoption, regulatory approvals, and technological development. Actual outcomes may differ materially.

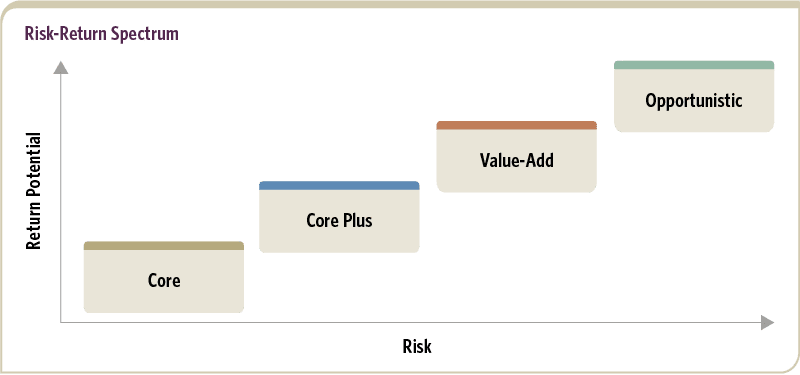

Different Investing Objectives Met with A Range of Risk/Reward

Infrastructure assets, while sharing common characteristics, vary greatly along the risk-return spectrum. For instance, the risk profile of a wind farm with a 20-year power purchase agreement differs considerably from that of a container terminal in a port. Additionally, understanding regulatory regimes is vital, as cash flows often come from regulated sources.

Given this diversity, infrastructure investments can offer varying levels of income, capital appreciation, and risk to suit investors’ specific risk, return, duration, and liquidity objectives. Like real estate, these assets are classified into one of four categories—core, core plus, value add, and opportunistic— each reflecting a different risk-return profile.

Core infrastructure investments are typically regulated, supported by the government, provide essential services, and thus are unlikely to experience prolonged outages. Utilities are a primary example. With monopolistic characteristics, they are the least risky of their peers, have stable cash flows, and the lowest yields and appreciation of the asset class.

Core plus assets have contractual, stable cash flows, moderate risk, with higher yields than core peers. They offer growth potential through expansion or acquisition. Examples of companies that provide energy under contracts include those offering thermal heating and cooling, and renewable-based electricity. Core plus assets seek to provide income with some capital gains.

Value-add assets carry more risk and typically undergo upgrades to increase market value, such as enhancements to capacity, operations, or intended use. These include enhancements such as capacity increases at ports, power plants, and data centers, or power plant upgrades to use cleaner fuel. Some assets may also have room for better contractual terms. Value-add assets seek to provide capital appreciation with some income.

Opportunistic infrastructure has the highest risk but also offers the greatest potential return. Generally, these assets are in development or restructuring, may use emerging technology such as hydrogen, and do not generate cash flows. Like private equity deals, these transactions seek to generate returns by identifying undervalued assets, improving their performance, and eventually selling them at a profit. Opportunistic assets have the shortest holding period, typically three to five years, and don’t provide income.

A Wide Spectrum of Risk and Return Targets

Source: Guggenheim Investments.

Chart is for illustrative purposes only. The strategies listed are organized based on Guggenheim Investments general view of each strategy’s potential risk and return opportunity relative to each other which is not a guarantee of future results. Over different time periods and market conditions the actual credit risk and return opportunity will be different based on the overall portfolio and strategy of each strategy and client account.

Infrastructure Investment Categories: Highlights and Risk Considerations

1. Core Infrastructure Investments

Stabilized, operating assets with long-duration contractual or regulatory revenue support, such as contracted renewable energy portfolios, rate-regulated utilities, long-term transportation concessions (roads, bridges, tunnels), essential-service water and wastewater systems, and fully leased data centers or fiber and broadband networks.

Potential Investment Highlights

Stable and regulated income: Revenue underpinned by long-duration contracts, regulated rate structures, or government concessions with investment-grade counterparties

Strong counterparties which can typically pass costs through to end users, supporting payment certainty

Limited volatility through commodity price swings, merchant power risk, or demand cyclicality

Proven operational track records with well-understood risk profiles

Key Risks

Regulatory or policy changes that could alter the economic framework supporting these assets

Re-contracting or concession renewal risk upon contract expiration, including repricing in a different market environment

Technology obsolescence over long holding periods

Concentration risk if portfolios are not sufficiently diversified across geography, counterparty, or asset type

Interest rate sensitivity, given long-duration stable cash flows

2. Core Plus Investments

Stable, cash-flowing assets with targeted growth or improvement opportunities, such as operational data centers with expansion capacity, telecom towers or fiber and broadband networks with tenant diversification potential, airports or seaports with usage-based upside, midstream energy infrastructure, district energy platforms, and social infrastructure under availability-based contracts.

Potential Investment Highlights

Blend of contractually secured income and growth potential through expansion, efficiency upgrades, or tenant diversification

Essential service assets supporting durable demand and high renewal rates

Exposure to favorable secular trends such as digitalization, electrification, and urbanization

Key Risks

Execution risk on expansion or improvement initiatives

Tenant or customer turnover creating near-term cash flow variability

Capital expenditure requirements that may not achieve projected returns

Greater economic cycle sensitivity relative to core assets

3. Value-Add Investments

Assets requiring active management, construction execution, or operational enhancement to realize full return potential, such as late-stage development power generation or industrial platforms with offtake agreements in place, seaports or airports undergoing capacity expansion, data centers in build-out with anchor tenants secured, rail or transit infrastructure requiring modernization, and water or environmental services platforms being consolidated or improved.

Potential Investment Highlights

Contracted or quasi-contracted cash flows providing downside support during construction or ramp-up

Captive customer dynamics or high switching costs supporting revenue durability

Contractual risk mitigation through cost pass-throughs, escalation provisions, and minimum volume commitments

Growth platform potential through adjacent expansion, new services, or complementary assets

Key Risks

Construction risk, including cost overruns and schedule slippage

Operational ramp-up or lease-up risk before reaching stabilized cash flows

Counterparty credit risk where revenue depends on a limited number of offtakers

Regulatory or permitting uncertainty affecting competitive positioning or viability

4. Opportunistic Investments

Development-stage or greenfield projects, assets in supply-constrained markets, or platforms requiring substantial capital deployment before generating stabilized cash flows, such as greenfield power generation or power transmission addressing capacity shortfalls, large-scale data center development, new-build transportation projects (roads, rail, seaports) in underserved markets, emerging technology platforms (e.g., hydrogen, carbon capture, advanced storage), distressed assets requiring restructuring, and new-build housing or social infrastructure.

Potential Investment Highlights

Strategic positioning in markets with demonstrated supply-demand imbalances or capacity constraints

Technology, efficiency, or location advantages supporting favorable competitive positioning

Potential first-mover advantages in rapidly growing or emerging infrastructure segments

Development milestones already achieved that partially de-risk execution

Key Risks

Full development and construction risk, including the possibility projects may not reach completion

Market and demand uncertainty, including future pricing, usage levels, or technology adoption rates

Financing risk given sensitivity to interest rate and credit market conditions

Technology risk from competing or next-generation alternatives

The Guggenheim Investments Approach to Infrastructure Investing

We believe that a significant capital shortfall in middle-market infrastructure investments presents a compelling opportunity for sophisticated investors. This gap may allow for favorable deal terms and potentially strong risk-adjusted returns. We strategically target middle-market projects (valued between $50 and $500 million), seeking to capitalize on the higher volume of opportunities and reduced competition. Our broad origination platform presents opportunities for us to source transactions outside traditional channels, including acquisitions, equity investments, and subordinated credit. When applicable, the less competitive subordinated credit market can potentially provide us with enhanced bargaining power and allows for robust covenant packages. Within this landscape, the most attractive real assets are often those driven by secular trends, requiring substantial investment and demonstrating resilience throughout economic cycles, rather than relying on interest rates or broader economic performance.

Our investment approach seeks to prioritize high quality partnerships and portfolio diversification across sectors and capital structures . We focus on essential services with high barriers to entry, low cyclicality, inflation linkage, and a current yield component. Supported by strong contractual frameworks, these investments are designed to withstand not only economic shocks but also technological, commodity, and disruption risks.

Guggenheim’s hard asset investment approach leverages our scale and deep underwriting expertise across dedicated infrastructure, real estate, and structured product franchises. This integrated team approach ensures thorough due diligence, tactical portfolio construction, and optimized relative value. Extensive industry relationships—including financial sponsors, deal brokers, and corporate credit platforms—provide differentiated investment opportunities, enabling us to target underserved sectors and unlock value with a focus on risk-adjusted returns. Our flexible capital structure approach further enhances our ability to execute complex transactions. With positions in over 1,500 companies and a vast industry network, Guggenheim is well-positioned to partner with investors seeking access to high quality assets and disciplined investment management.

Important Notices and Disclosures

Infrastructure investing is subject to a number of risks, including:

No Guarantee of Returns. Infrastructure investments are subject to market volatility and there is no guarantee that any investment objective will be achieved. Past performance is not indicative of future results. You may lose some or all of your invested capital.

Illiquidity Risk. Infrastructure investments, particularly in private markets, are generally illiquid. Investors may be unable to sell or exit their investment for an extended period, potentially years. There may be no secondary market for these investments, and redemption rights may be limited or nonexistent.

Regulatory and Political Risk. Infrastructure assets are often subject to extensive government regulation, including rate-setting, environmental compliance, permitting requirements, and potential changes in law or policy. Changes in the regulatory environment, government administration, or political priorities may adversely affect the value and operation of infrastructure investments.

Concentration Risk. Infrastructure investments may be concentrated in specific sectors (e.g., energy, transportation, utilities) or geographic regions. This concentration may increase volatility and the potential for loss compared to more diversified investments.

Operational Risk. Infrastructure assets require ongoing management, maintenance, and capital expenditure. Operational failures, cost overruns, construction delays, labor disputes, or technological obsolescence could negatively impact investment returns.

Interest Rate Risk. Infrastructure investments, particularly those with stable, bond-like cash flows, may be sensitive to changes in interest rates. Rising interest rates may reduce the relative attractiveness of infrastructure returns and negatively impact valuations.

Inflation Risk. While certain infrastructure assets may offer inflation protection, there is no guarantee that revenues or contractual adjustments will fully offset the effects of inflation on operating costs or investment returns.

Leverage Risk. Infrastructure investments may employ significant leverage (borrowed capital) to finance acquisitions or operations. Leverage amplifies both gains and losses and may increase the risk of default or insolvency.

Valuation Risk. Private infrastructure assets are not publicly traded and may be difficult to value accurately. Valuations may be based on estimates, assumptions, or models that may prove incorrect, and actual realizable value upon sale may differ materially from stated valuations.

Environmental and Climate Risk. Infrastructure assets may be exposed to physical climate risks (extreme weather, rising sea levels, natural disasters) and transition risks (policy changes, carbon pricing, shifts in energy demand). These factors may result in asset impairment, increased costs, or stranded assets.

This material is distributed or presented for informational or educational purposes only and should not be considered a recommendation of any particular security, strategy, or investment product, or as investing advice of any kind. This material is not provided in a fiduciary capacity, may not be relied upon for or in connection with the making of investment decisions, and does not constitute a solicitation of an offer to buy or sell securities. The content contained herein is not intended to be and should not be construed as legal or tax advice and/or a legal opinion. Always consult a financial, tax and/or legal professional regarding your specific situation.

This material contains opinions of the author, but not necessarily those of Guggenheim Partners, LLC, or its subsidiaries. The opinions contained herein are subject to change without notice. Forward looking statements, estimates, and certain information contained herein are based upon proprietary and non-proprietary research and other sources. Information contained herein has been obtained from sources believed to be reliable, but are not assured as to accuracy. Past performance is not indicative of future results. There is neither representation nor warranty as to the current accuracy of, nor liability for, decisions based on such information.

©2026, Guggenheim Partners, LLC. No part of this article may be reproduced in any form, or referred to in any other publication, without express written permission of Guggenheim Partners, LLC.

Guggenheim Funds Distributors, LLC an affiliate of Guggenheim Partners, LLC. For more information, visit guggenheiminvestments.com or call 800.345.7999.

Not FDIC Insured | Not Bank Guaranteed | May Lose Value

TL-PS-RA 5263251

Portfolio Management Outlook: Staying Focused Amid Geopolitical Uncertainty

Investing in Private Debt